Are Facebook or PayPal Donations Considered Foreign Contributions?

Overview

The advent of digital platforms like Facebook and PayPal has revolutionized fundraising, enabling NGOs to tap into global donor networks with unprecedented ease. However, these platforms introduce complexities under the Foreign Contribution (Regulation) Act, 2010 (FCRA), which meticulously regulates the inflow of foreign contributions to ensure they align with Indias national interests. The classification of donations received through these platforms hinges on the donors identity and nationality, not the medium of transfer. Contributions from foreign sources such as non-Indian citizens, foreign entities, or Non Resident Indians (NRIs) with foreign nationality are unequivocally classified as foreign contributions, necessitating FCRA registration or prior permission. Conversely, donations from Indian citizens, including NRIs retaining Indian citizenship, are exempt unless they exceed Rs. 1,00,000, requiring reporting via Form FC-1. NGOs must navigate these nuances with precision to avoid severe penalties and maintain their legal standing.

Statutory Framework

Section 2(1)(h) of the FCRA, 2010, defines foreign contribution as any donation, delivery, or transfer made by a foreign source, including currency, securities, or articles. This encompasses donations from non-Indian citizens, foreign companies, or NRIs with foreign nationality, regardless of the platform used. Contributions from Indian citizens abroad, made through personal savings via normal banking channels, are not treated as foreign contributions unless they exceed Rs. 1,00,000, as per the Foreign Contribution (Regulation) Second Amendment Rules, 2019. Section 11 mandates that NGOs obtain registration or prior permission to accept such contributions, with violations punishable under Sections 3335, including fines, fund seizure, and imprisonment up to five years. The Income Tax Act, 1961, further complicates the scenario, as unauthorized foreign contributions may be taxable under Section 2(24) if they do not qualify for Section 11 exemptions.[ (https://taxguru.in/corporate-law/foreign-contribution faq.html) [] (https://taxguru.in/corporate-law/frequently-asked-questions-faqs-fcra.html)

Legal and Tax Implications

Donations via Facebook or PayPal from foreign sources require FCRA registration and must be deposited in a designated FCRA account at the State Bank of India, New Delhi Main Branch. Non-compliance, such as accepting funds in a non-designated account, invites penalties, including seizure of funds and potential tax liabilities under the Income Tax Act. For instance, donations exceeding Rs. 1,00,000 from an NRI with Indian citizenship must be reported within 30 days using Form FC-1, failing which the NGO risks penalties. The 2020 FCRA amendments tightened oversight, mandating that all foreign contributions be routed through the SBI account, with banks reporting transactions to the MHA. NGOs must verify donor nationality and maintain meticulous records to ensure compliance and avoid legal repercussions.

Judicial and Regulatory Insights

The 2020 FCRA amendments emphasized stringent oversight of foreign contributions, clarifying that donations from OCIs are foreign contributions, requiring FCRA compliance. The Supreme Courts 2022 ruling upholding these amendments reinforced the need for transparency in foreign funding, highlighting the MHAs authority to scrutinize digital transactions. Cases like the 2017 suspension of the Public Health Foundation of Indias FCRA registration for alleged misuse of funds underscore the governments vigilance over foreign contributions, including those received through digital platforms. These precedents emphasize the importance of robust compliance mechanisms.[](https://www.thehindu.com/news/national/the hindu-explains-what-is-foreign contribution-regulation-act-and-how-does-it-control-donations/article32590504.ece)[](https://cof.org/news/new indian-fcra-amendments-impact-foreign-grants-indian-ngos).

Practical Scenarios

Consider an NGO receiving a Rs. 2 lakh donation via PayPal from a U.S.-based donor.Without FCRA registration, the funds are seized, and the donation is taxed as income under the Income Tax Act. In another scenario, an FCRA-registered NGO accepts a Rs. 50,000 donation from an NRI with Indian citizenship via Facebook, which is exempt from FCRA as it falls below the Rs. 1,00,000 threshold. However, if the same NRI donates Rs. 1.5 lakhs, the NGO must report it via Form FC-1 within 30 days, or face penalties. A third case involves an NGO accepting a PayPal donation in a non-FCRA account, leading to fund seizure and a fine for violating the designated account requirement.

Common Pitfalls and Mitigation Strategies

A frequent error is assuming digital donations are exempt from FCRA due to their platform-based nature, leading to unauthorized acceptance and penalties. NGOs can mitigate this by verifying donor nationality before accepting funds. Another pitfall is depositing foreign contributions in non-designated accounts, violating FCRA mandates. Opening and exclusively using an SBI FCRA account prevents this. Inadequate documentation of donor details also invites scrutiny; NGOs should maintain comprehensive records of donor identity, nationality, and transaction details. Regular audits and legal consultations can further safeguard compliance.

Professional Recommendations

NGOs should verify donor nationality through passports or OCI cards to confirm whether donations are foreign contributions. Obtaining FCRA registration or prior permission is essential for accepting funds from foreign sources. All contributions must be routed through the designated SBI FCRA account, with banks reporting transactions to the MHA. Maintaining detailed records of all digital donations and engaging legal experts to navigate FCRA complexities are critical. Regular audits ensure transparency and compliance, protecting NGOs from penalties and enhancing donor trust.

Conclusion

Donations via Facebook or PayPal are classified as foreign contributions if they originate from foreign sources, requiring FCRA registration and adherence to strict compliance protocols. NGOs must verify donor identity, use designated accounts, and maintain robust documentation to avoid penalties and tax liabilities. By prioritizing compliance and transparency, NGOs can leverage digital platforms to expand their funding while safeguarding their legal and financial integrity.

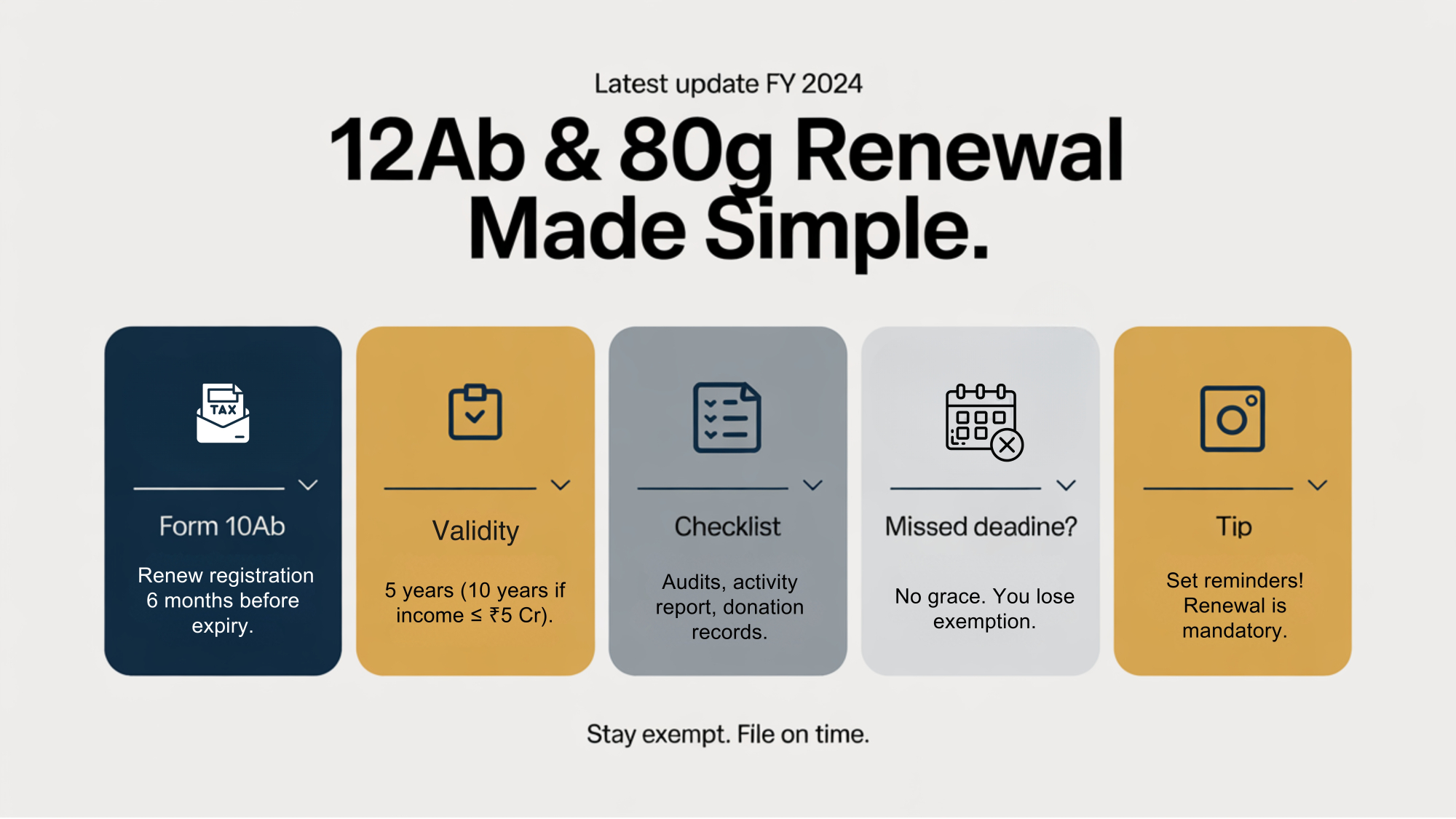

Latest Rules for Renewal of 12AB & 80G Registrations Under current tax law, registe...

Taxation of AOP (Association of Persons) Based on Member Share Determinability 1. Where Share of...

What Constitutes “Charitable Purpose” Under Section 2(15)– Judicial Trends and M...

Remuneration to Trustees: When Is It Permissible Under Law? Legal Framework and Bare Act Analy...

FCRA Renewal Process: Timeline, Documents, and Grounds for Rejection Overview The FCR...

Treatment of Foreign Services Online Courses, Webinars by NGOs FCRA Risk Overview T...

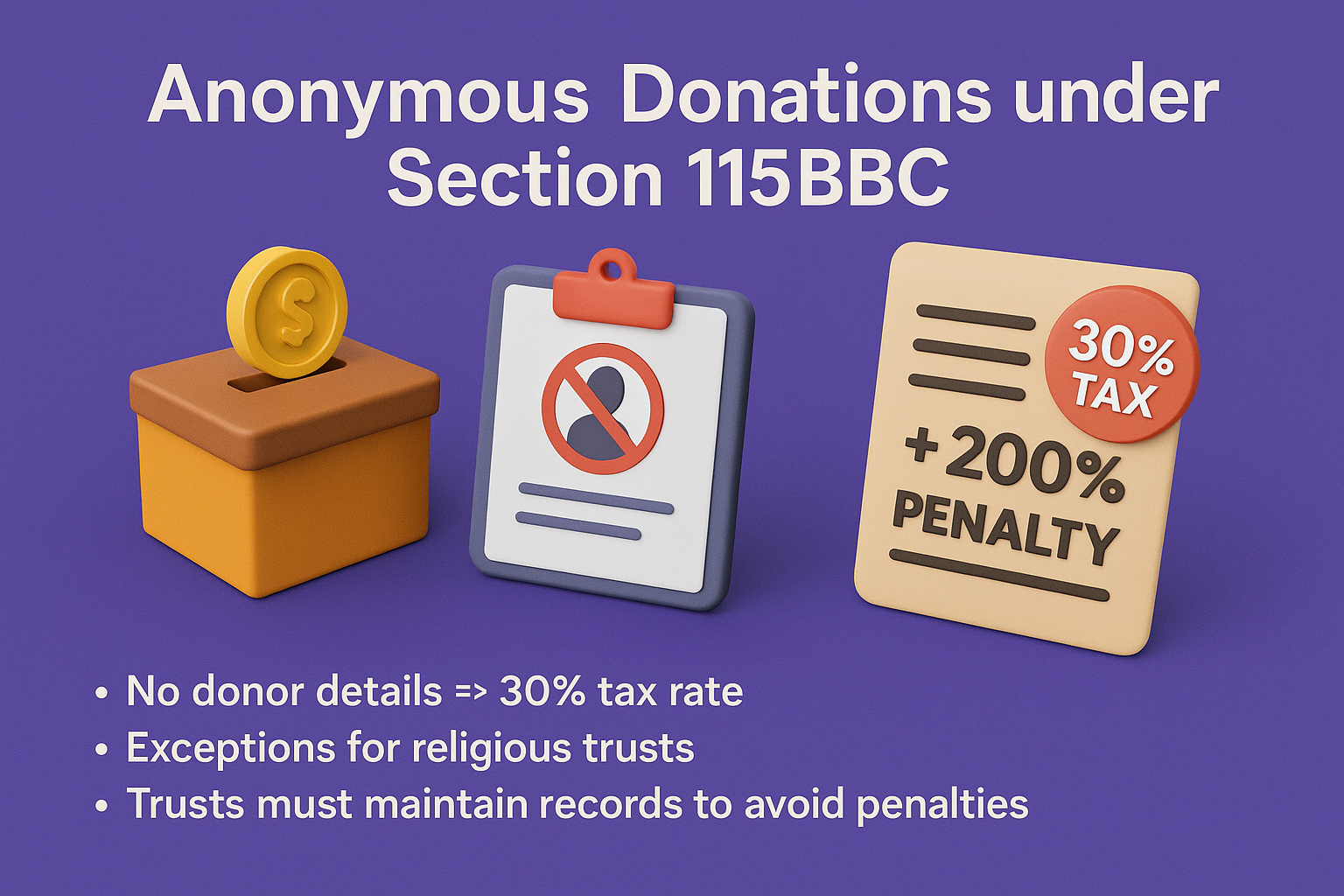

Anonymous Donations under Section 115BBC – Rules, Limits & Penalties Definiti...

.png)

Impact of Mandatory Aadhaar Linking for NGO Trustees – Legal Validity & Privacy Concer...

FCRA Bank Account Designated vs Utilization Account Clarified Overview The FCRA, 2010...

New Income Tax Return Filing Requirements for NGOs – Form ITR-7 Explained Legal Framewo...