Should Political Funding Be Allowed Through NGOs? – Legal Loopholes, Risks & Reforms

Introduction

The intersection of NGOs and political funding in India is a highly contentious arena, fraught with legal ambiguities, ethical dilemmas, and potential for misuse. NGOs, traditionally viewed as apolitical entities dedicated to advancing social welfare, face intense scrutiny when their activities encroach upon political spheres. The debate over whether NGOs should be permitted to fund political parties, particularly through domestic donations or CSR contributions, hinges on a delicate balance between fostering democratic participation and mitigating risks such as diversion of charitable funds, undue political influence, and erosion of organizational autonomy. This section provides a comprehensive analysis of the legal framework, identifies loopholes, assesses risks, evaluates competing perspectives, and proposes actionable reforms to ensure transparency and accountability in this sensitive domain.

Legal Framework

The legal framework governing NGOs and political funding in India is multifaceted, encompassing several statutes that regulate the receipt, utilization, and reporting of funds:

Case Study: In 2015, Greenpeace India’s FCRA registration was revoked by the Ministry of Home Affairs (MHA) for allegedly using foreign funds to support political advocacy against government policies, such as protests against nuclear and coal projects. This case underscores the government’s stringent enforcement of FCRA provisions to curb political activities by NGOs, even when framed as public interest advocacy.

Legal Loopholes

The absence of an explicit prohibition on domestic political funding by NGOs creates significant loopholes. While foreign contributions are tightly regulated under the FCRA, NGOs could potentially channel domestic funds—such as those received through CSR, individual donations, or fundraising campaigns—to political parties under the guise of advocacy or public welfare initiatives. For example, an NGO might fund a campaign promoting a political party’s agenda by labeling it as a public awareness program, exploiting the lack of specific regulations. The 2018 FCRA amendment, which permitted foreign companies with Indian subsidiaries to fund political parties, further complicates the landscape, as NGOs might indirectly facilitate such funding through corporate partnerships or collaborative projects. Additionally, the lack of mandatory disclosure requirements for NGO political contributions exacerbates transparency concerns, allowing funds to flow without public or regulatory oversight.

Risks and Concerns

Permitting NGOs to fund political parties, even with domestic funds, poses several risks that could undermine their mission and the broader democratic process:

Undue Political Influence: Large donations from NGOs could sway political outcomes, leading to policies that favor donor interests over public welfare, a concern amplified by the opacity of funding channels like electoral bonds.

Transparency Issues: Without mandatory disclosure of political contributions, the sources and destinations of funds remain obscure, fostering suspicions of illicit funding and reducing accountability

Loss of Organizational Autonomy: NGOs risk becoming proxies for political agendas, compromising their independence and credibility as impartial actors dedicated to social good.

Legal and Regulatory Ambiguities: The lack of clear guidelines creates uncertainty, exposing NGOs to legal challenges, deregistration, or reputational damage if their activities are deemed political.

Example: Consider “Empower India,” an NGO focused on rural education. If it channels 10 lakhs from its domestic donations to a political party’s campaign under the pretext of an educational awareness drive, it risks diverting resources from classroom programs, violating its charitable mandate, and facing scrutiny from tax authorities.

Debate: Should Political Funding Be Allowed?

The debate over political funding through NGOs involves a complex interplay of democratic principles, ethical considerations, and regulatory challenges:

Arguments in Favor of Allowing Political Funding:

Arguments Against Allowing Political Funding:

Reforms and Solutions

To address the risks and loopholes associated with political funding by NGOs, the following reforms are proposed to ensure a balanced approach:

Example: Implementing a mandatory disclosure system akin to the ECI’s requirement for political parties to report contributions above 20,000 could enhance transparency if extended to NGOs. For instance, “Empower India” would need to disclose any political contributions in its Form FC-4 or income tax returns, ensuring public accountability.

Table 1: Political Funding by NGOs: Key Considerations

| Aspect | Details |

| Legal Restrictions | FCRA prohibits foreign funds for political activities; domestic funding ambiguous |

| Risks | Misuse of funds, political influence, transparency issues, autonomy loss |

| Proposed Reforms | Clear laws, mandatory disclosures, enhanced ECI oversight, public funding |

Recent Updates (2025)

As of June 4, 2025, the Supreme Court’s February 2024 ruling declaring the electoral bond scheme unconstitutional has heightened scrutiny on political funding transparency, emphasizing the need for robust disclosure mechanisms. While this ruling does not directly address NGO contributions, it sets a precedent for increased accountability, which could influence future regulations governing NGO political funding. Additionally, the MHA’s extension of FCRA registration validity until June 30, 2025, provides temporary relief for NGOs but underscores ongoing regulatory vigilance over their activities.

Conclusion

The debate over political funding through NGOs in India reflects a tension between fostering democratic participation and preserving the charitable mandate of NGOs. While legal loopholes permit potential misuse of domestic funds, the risks of political influence, transparency issues, and loss of autonomy necessitate urgent reforms. Clear legislation, mandatory disclosures, enhanced oversight, and increased public funding for elections can ensure that NGOs remain true to their mission while contributing to a transparent and equitable political funding ecosystem.

)%20(1).jpg)

Understanding Religious Trusts Under Indian Law and Income Tax Act Religious trusts in India pla...

Form 10BD and 80G Compliance Legal Framework Section 80G(5)(viii) of the Income Tax A...

.png)

EPF in India is a retirement savings scheme managed by EPFO under the Ministry of Labour and Empl...

).jpg)

Unregistered Trusts under the Income Tax Act, 1961 Legal Framework for Unregistered Trusts ...

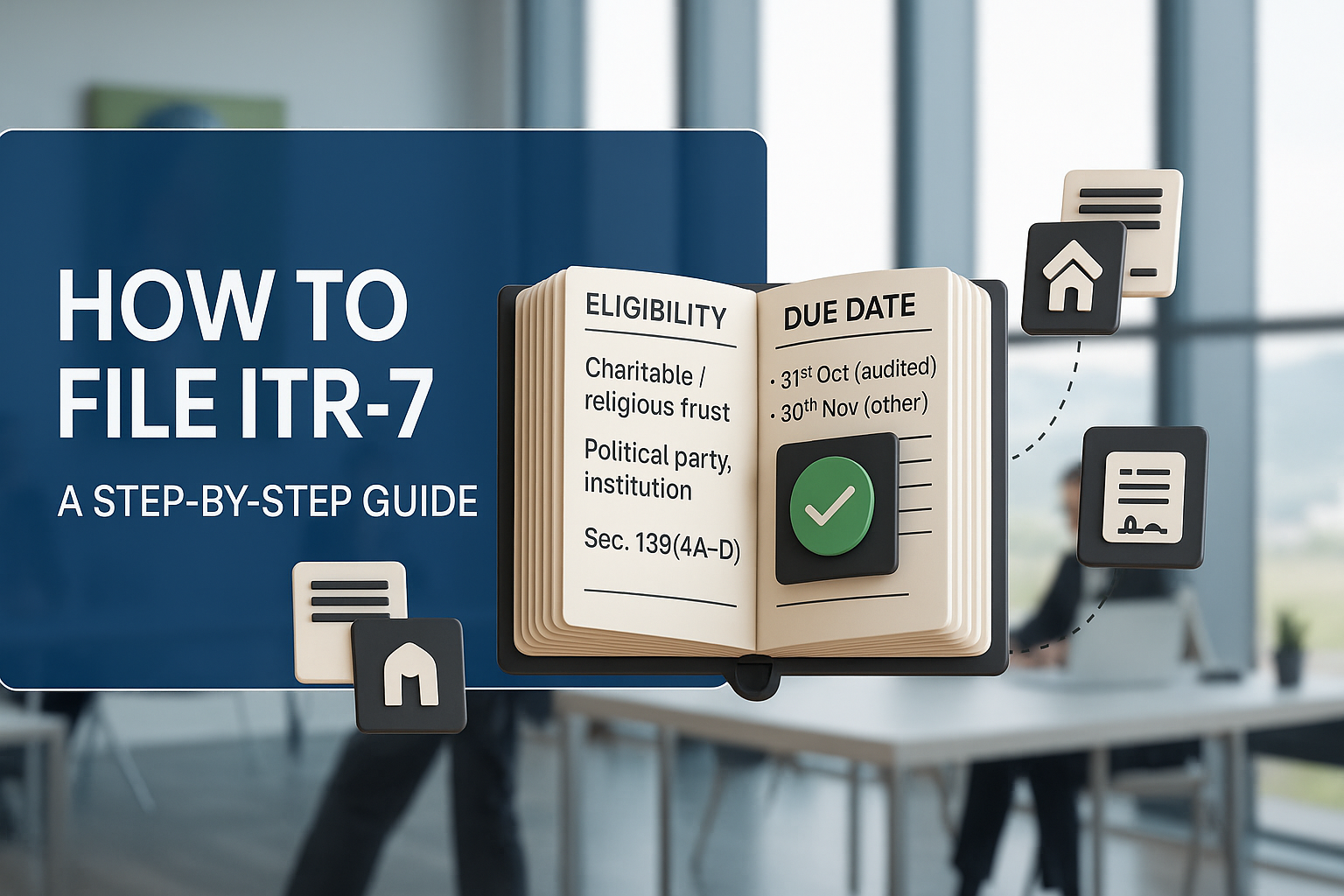

How to File ITR-7: A Step-by-Step Guide Who Must File. ITR-7 is the Income-tax return f...

).jpg)

Government Grants: An Exhaustive Analysis Under Income Tax Law and Ind AS Framework Government...

Taxation of AOP (Association of Persons) Based on Member Share Determinability 1. Where Share of...

A Complete Guide to Legal Structure, Registration, and Taxation of NPOs in India Introduction ...

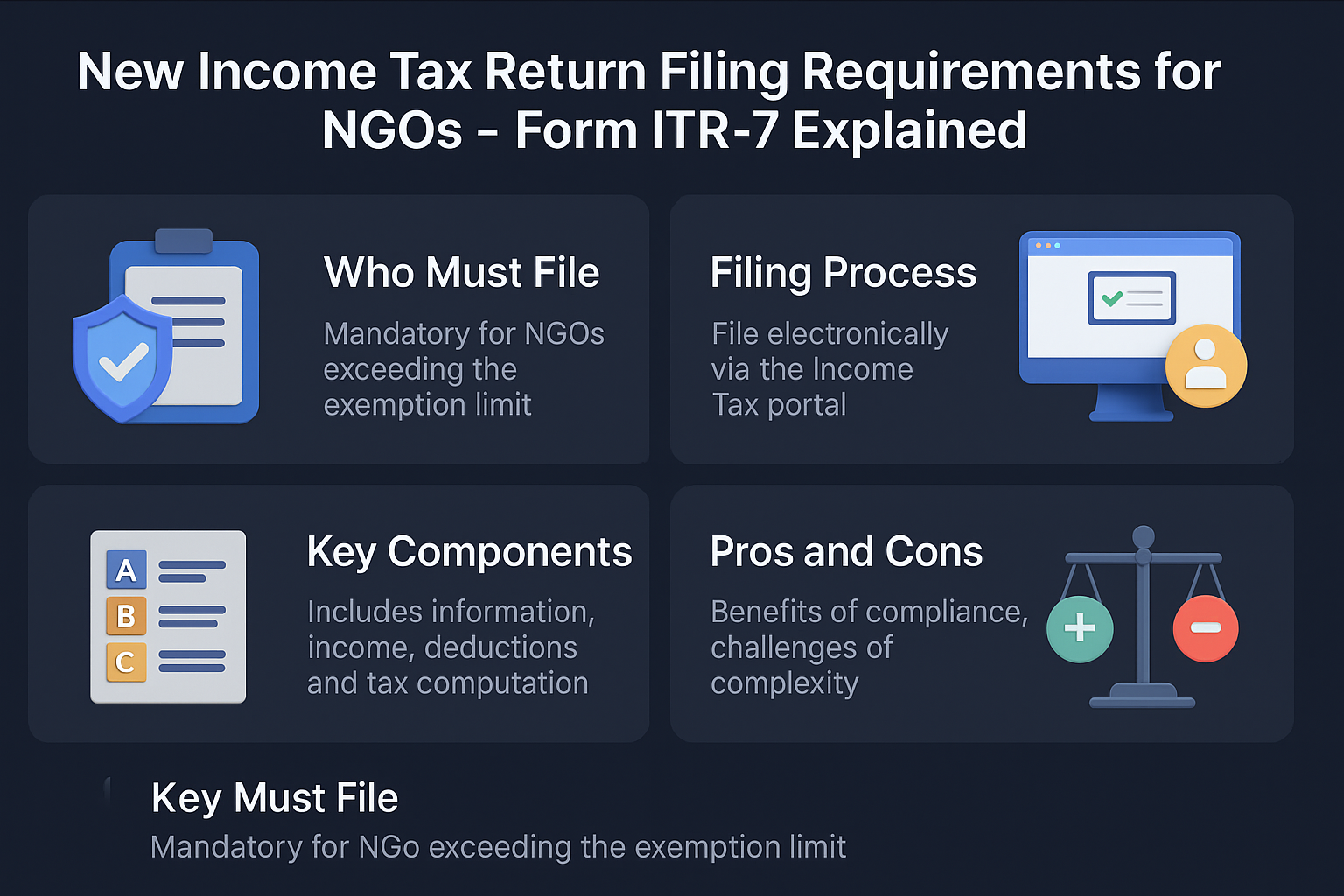

New Income Tax Return Filing Requirements for NGOs – Form ITR-7 Explained Legal Framewo...

Charitable Organisations – Taxation & Compliance (Legal Research Guide) Th...