Difference Between Voluntary Contributions, Corpus Donations, and Anonymous Donations

Introduction

Donations are the financial backbone of NGOs, enabling them to fund operations and programs. However, their tax treatment under the Income Tax Act, 1961, varies significantly, depending on their nature and purpose, impacting an NGO’s financial planning and compliance obligations. Understanding the distinctions between voluntary contributions, corpus donations, and anonymous donations is crucial for optimizing tax exemptions and ensuring accurate reporting. This section provides a comprehensive analysis of the definitions, tax treatments, legal requirements, and management practices for these donation types, highlighting their implications for NGOs.

Voluntary Contributions

Difference Between Trust, Society, and Section 8 Company Selecting the right NGO structure (Trus...

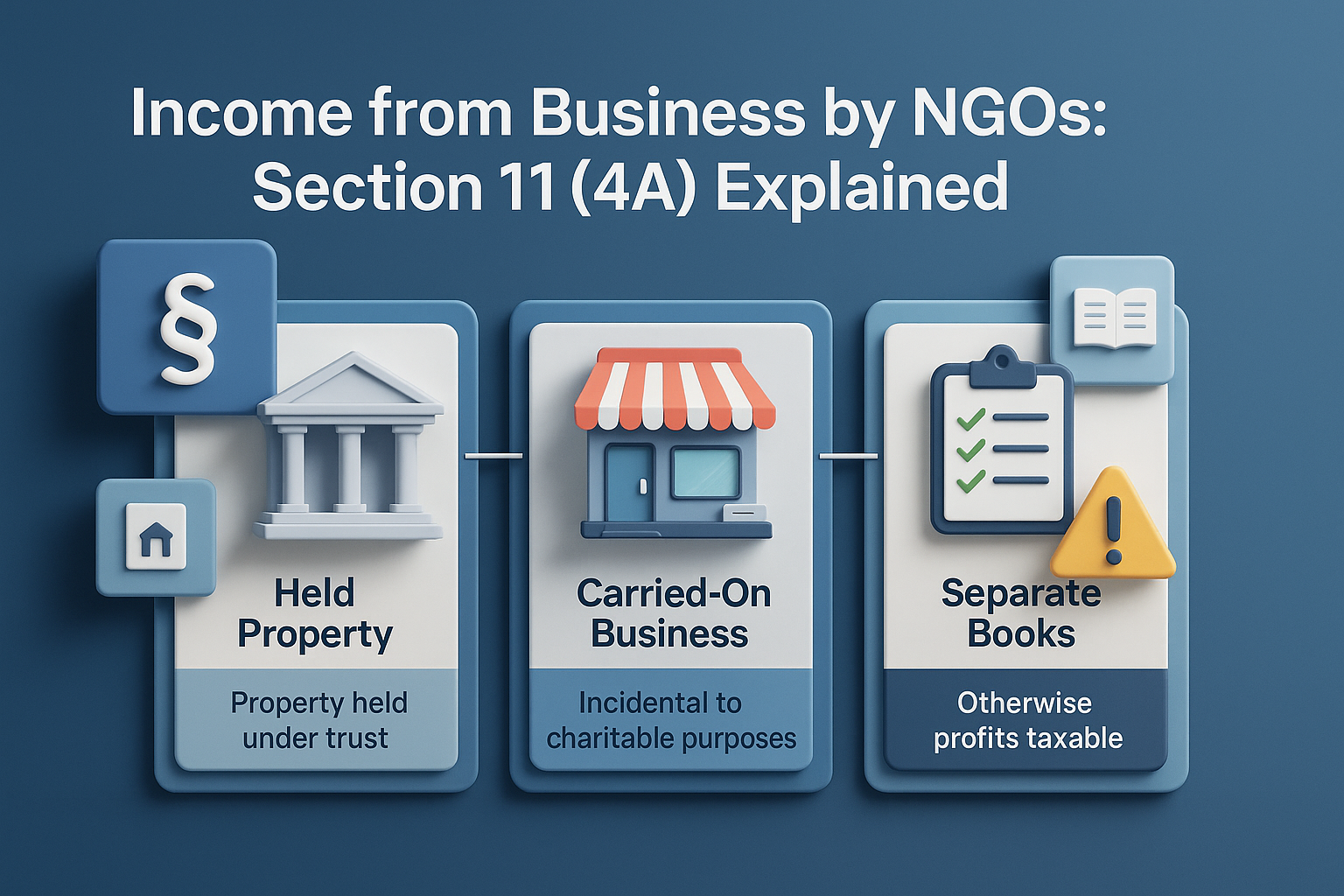

Income from Business by NGOs: Section 11(4A) Explained Legal Framework (Sections 11(4) and 11(4A...

A Complete Guide to Legal Structure, Registration, and Taxation of NPOs in India Introduction ...

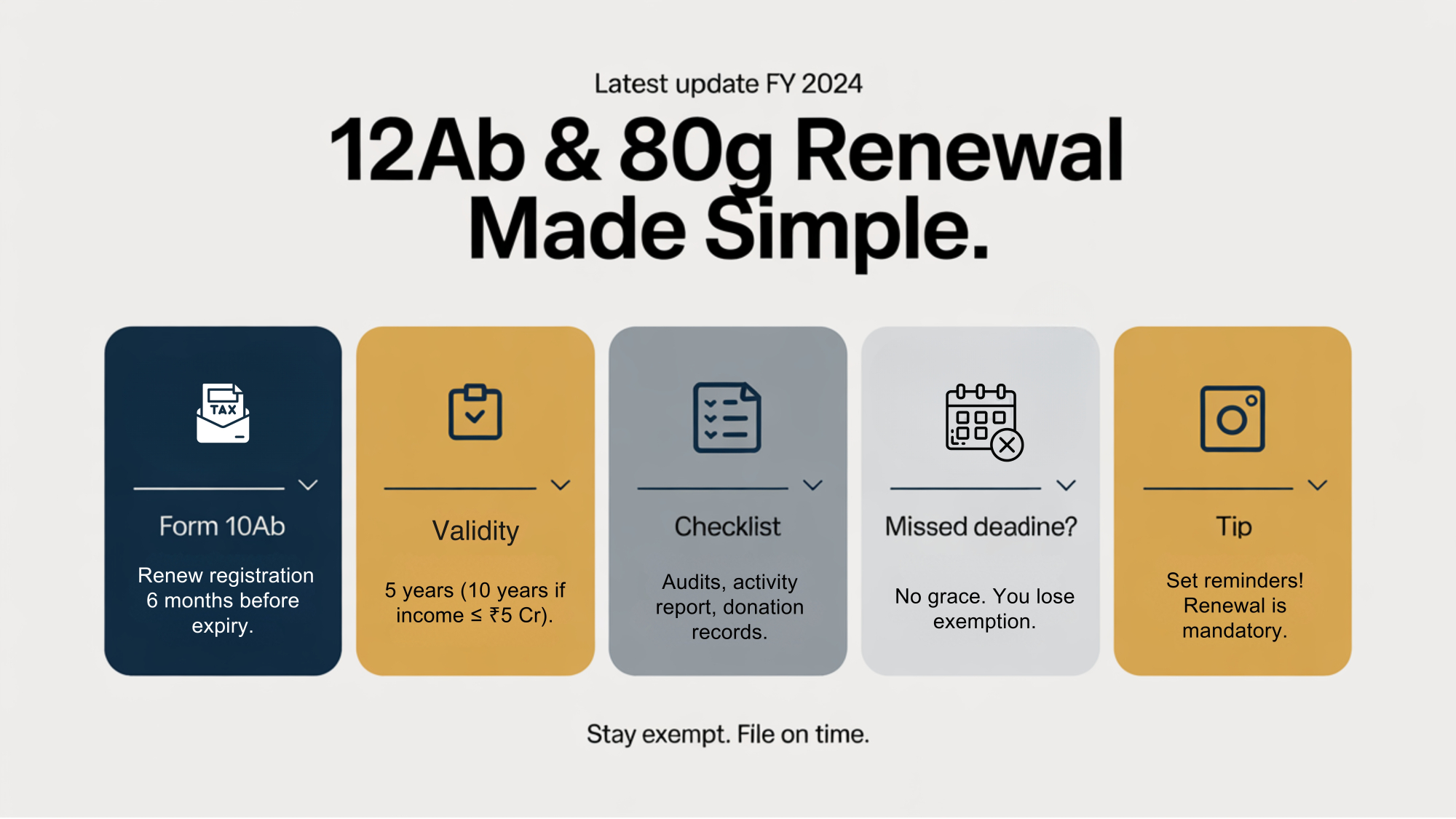

Latest Rules for Renewal of 12AB & 80G Registrations Under current tax law, registe...

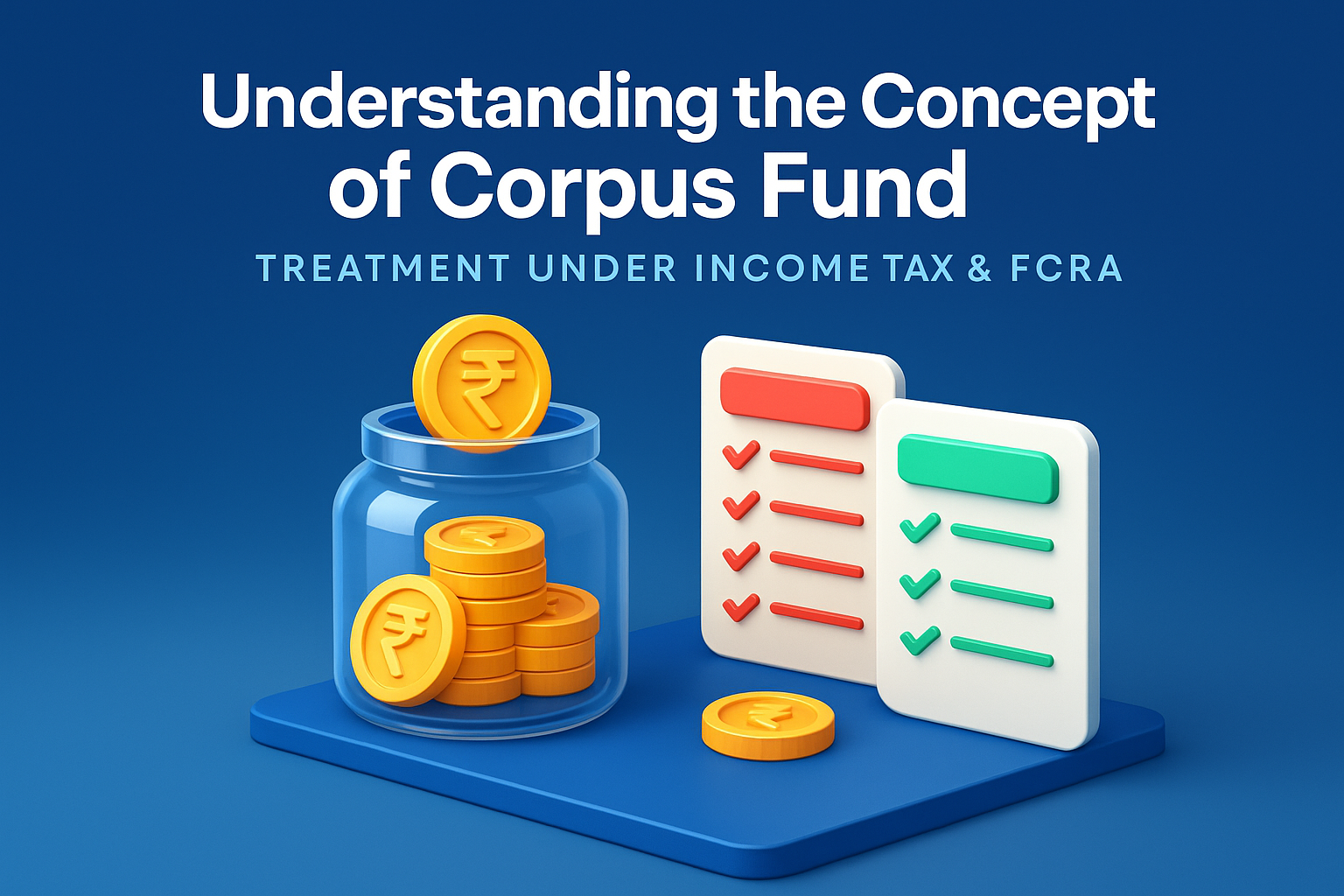

Understanding the Concept of Corpus Fund – Treatment Under Income Tax & FCRA ...

.png)

The rules and regulations that govern the functioning and operations of an Association of Persons ...

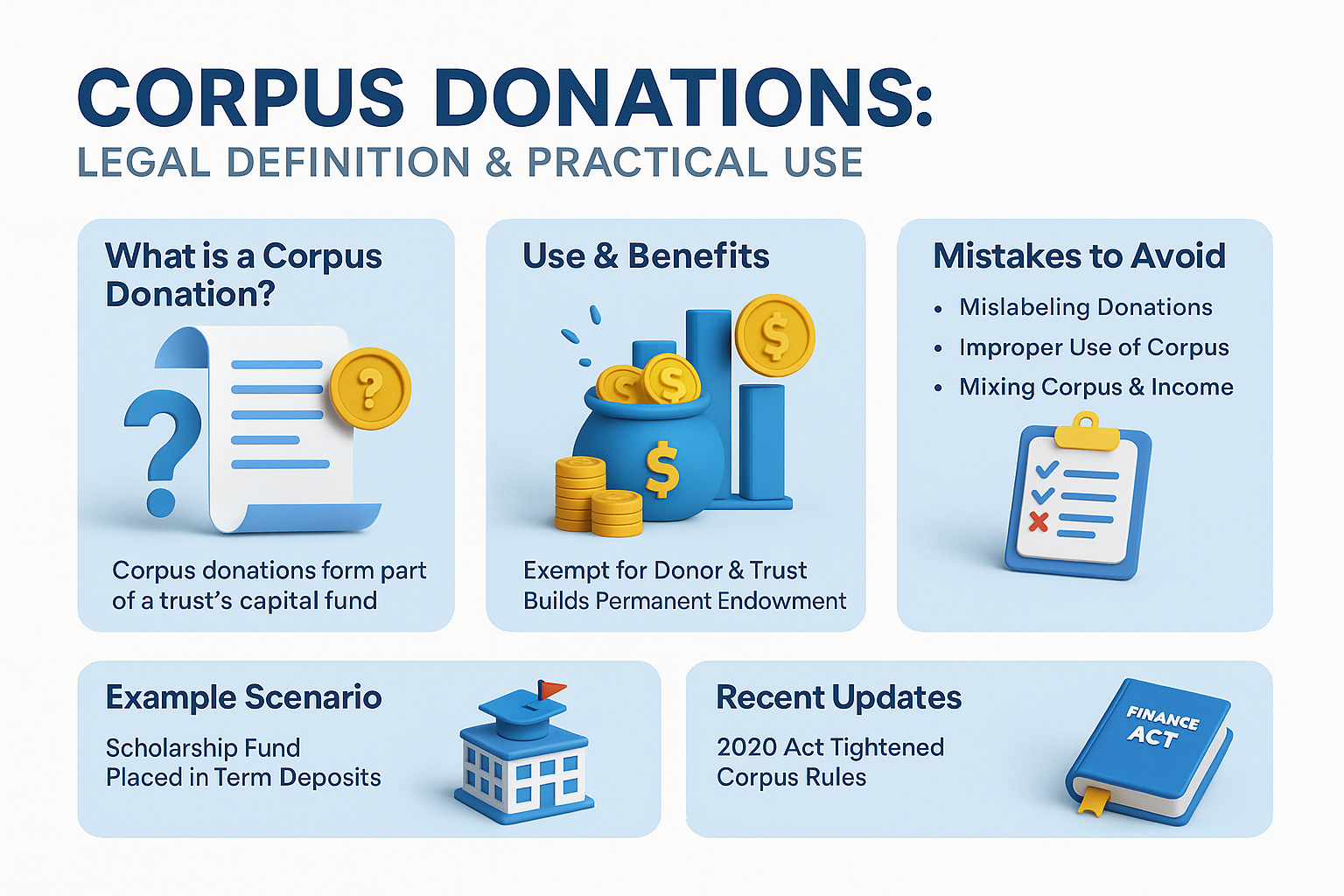

Corpus Donations: Legal Definition & Practical Use What is a Corpus Donation? A c...

)%20(1)(1).png)

Is GST Registration Required for Section 8 Companies? With the introduction of the Goods and Ser...

).jpg)

Unregistered Trusts under the Income Tax Act, 1961 Legal Framework for Unregistered Trusts ...

Social Stock Exchanges 1.1 Background We often feel like helping t...