How to Treat Donations in Kind–

Whether They Are Taxable or Exempt

Overview

Donations in kind, such as food, clothing, or services, are common for NGOs but lack clear statutory guidance on tax treatment. This section explores their treatment for donors and NGOs.

Tax Treatment for Donors

Under Section 80G, donors can claim deductions for cash donations to approved NGOs, but in-kind donations (e.g., clothes, food) are ineligible (Tax2win). Cash donations exceeding Rs. 2,000 are also ineligible unless made through banking channels.

Tax Treatment for NGOs

Section 2(24)(iia) includes voluntary contributions as income, potentially encompassing in-kind donations if converted to monetary value. If NGOs sell donated goods, the proceeds are taxable as income. If used directly for charitable purposes (e.g., distributing food), they are likely exempt, though no specific circular confirms this (IndiaIsUs).

Accounting and Reporting

NGOs must:

• Record in-kind donations at fair market value.

• Document their use (e.g., distribution or sale).

• Report all donations in annual returns to the Income Tax Department.

International Perspectives

Practical Considerations

NGOs should consult tax professionals to determine the taxability of in-kind donations and ensure proper accounting to avoid disputes with tax authorities.

Conclusion

NGOs in India must navigate complex tax provisions under Sections 2(15), 115BBC, and related sections to maintain exemptions and manage liabilities. Understanding judicial trends, maintaining records, and seeking professional advice are crucial for compliance. Thelack of clarity on in-kind donations highlights the need for further legislative guidance.

Summary of Key Tax Provisions for NGOs

| Provision | Key Features | Implications for NGOs |

| Section 2(15) | Defines charitable purpose; excludes commercial activities unless incidental and within 20% receipt limit. | Align activities with public benefit; maintain separate books for commercial activities. |

| Section 115BBC | Taxes anonymous donations at 30% if exceeding 5% of total do nations or Rs. 1 lakh. | Maintain donor records; limit anonymous donations. |

| Donations in Kind | Ineligible for donor deductions; taxable for NGOs if sold, likely exempt if used for charity. | Record fair market value; document use; seek professional ad vice. |

Introduction: Section 8 Companies, a distinctive provision under the Companies Act, 2013, embody ...

Income from Business by NGOs: Section 11(4A) Explained Legal Framework (Sections 11(4) and 11(4A...

.jpg)

How to Apply for CSR Registration on MCA Portal Under Section 135 of the Companies Act and the C...

Social Stock Exchanges 1.1 Background We often feel like helping t...

Private trusts and family trusts are like magical shields that protect your money and property. Th...

.png)

Impact of Mandatory Aadhaar Linking for NGO Trustees – Legal Validity & Privacy Concer...

Tax Basics: The tax rules for private trusts are laid out in Sections 160 to 164 of the Incom...

).jpg)

Step-by-Step Guide to Registering a Charitable Trust in India A charitable trust is a legal arra...

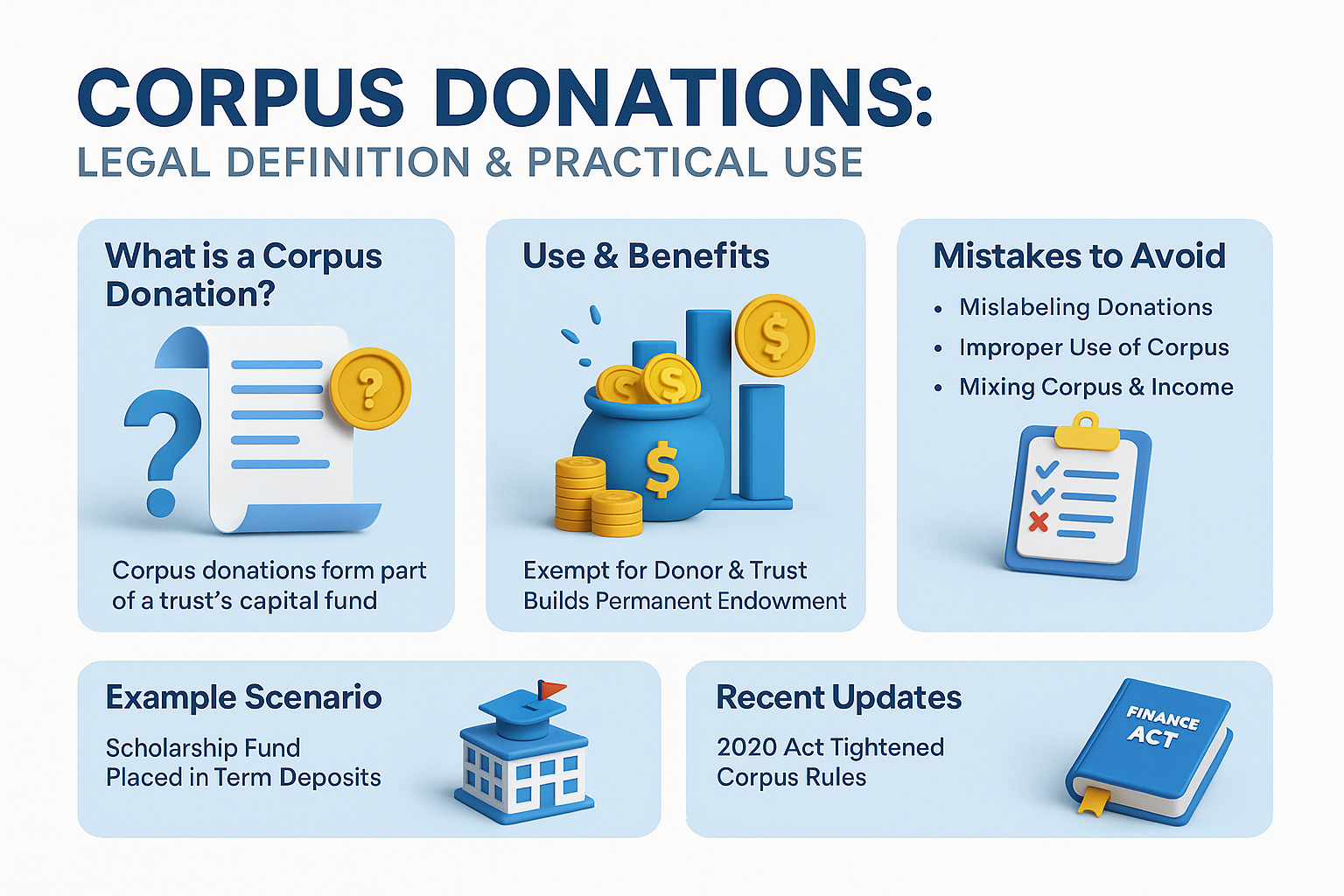

Corpus Donations: Legal Definition & Practical Use What is a Corpus Donation? A c...

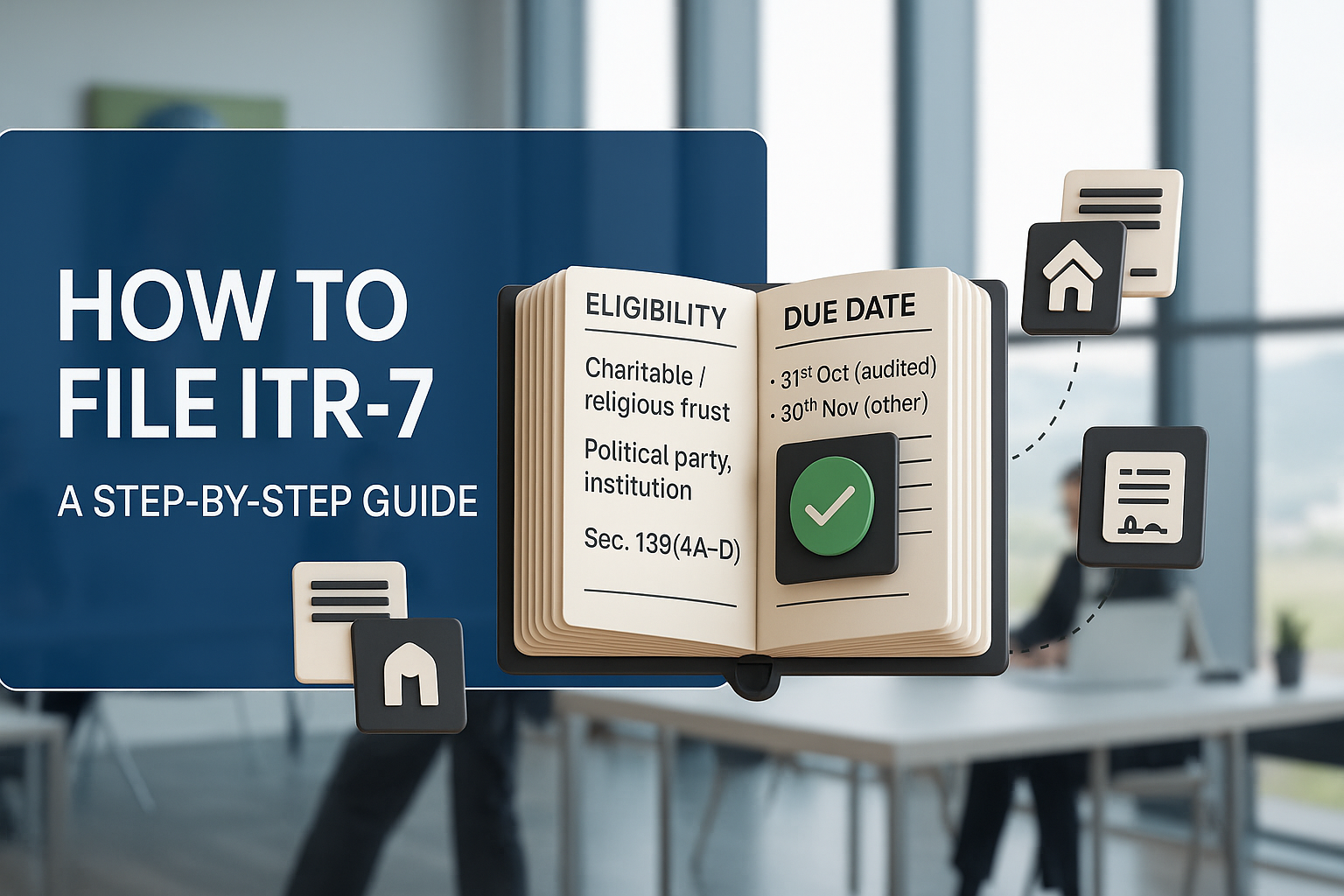

How to File ITR-7: A Step-by-Step Guide Who Must File. ITR-7 is the Income-tax return f...