Private trusts serve as powerful tools for asset management and wealth preservation, but understanding their scope, limitations, and the essential components like trust deeds is crucial for their effective operation.

Let's delve into the intricacies of private trusts and shed light on their creation, governance, and legal aspects.

Scope and Restrictions of Private Trusts:

1. Adherence to Trust Deed: A trust must abide by the guidelines set forth in its trust deed. Any activities prohibited by the trust deed cannot be carried out by the trust.

2. Tax Implications: Income generated from business activities conducted by a trust is subject to taxation at the Maximum Marginal Rate (MMR) under the Income Tax Act. This underscores the importance of careful planning and adherence to legal requirements.

3. Asset Transfer and Beneficiary Benefits: Assets cannot be transferred to trustees or used for the benefit of trustees unless they are also beneficiaries of the trust. This ensures transparency and prevents conflicts of interest.

4. Prohibition of Personal Profit: Trustees are prohibited from personally profiting from the funds of the trust. However, they may be entitled to management fees as outlined in the trust deed for their services.

5. Duration of Trust: A private trust can be established for a specific period or perpetually, depending on the settlor's intentions and objectives.

6. Creation Through Will: Private trusts can also be created through a will, wherein the estate is transferred to a trust for the benefit of family members. This transfer is not taxable under Section 56(2)(x) of the Income Tax Act.

Understanding Trust Deeds:

A trust deed is a crucial document that outlines the terms, conditions, and governance structure of the trust. It typically includes the following components:

1. Name of the Trust: The official name by which the trust will be known.

2. Parties Involved: This includes the name of the settlor, initial trustees, and beneficiaries.

3. Scope of Operations: The geographical area or jurisdiction within which the trust will operate.

4. Objects: The objectives or purposes for which the trust is established.

5. Duties and Powers of Trustees: The responsibilities and authorities granted to the managing trustees for the administration of the trust.

6. Residuary Clause: Provisions for the distribution of remaining assets in the event of trust dissolution or completion of objectives.

7. Dissolution: Procedures and conditions for the termination or dissolution of the trust.

8. Signatures: Signatures of trustees and witnesses to authenticate the trust deed.

Trust Creation Through Will:

Creating a trust through a will involves complying with the Indian Succession Act, 1925.

The testator must be of

sound mind and make the will freely, without coercion or fraud.

While registration of the will is not mandatory, it is advisable to prevent future disputes. In conclusion, understanding the intricacies of private trusts, including their scope, restrictions, and trust deeds, is essential for their effective establishment and management. Whether created independently or through a will, private trusts offer a robust mechanism for asset protection and succession planning.

Anonymous Donations and Tax Liability Under Section 115BBC– What NGOs Must Know S...

Complete Guide to Form 10A and 10AB– New Compliance Framework for 12AB Registration &nbs...

Tax Basics: The tax rules for private trusts are laid out in Sections 160 to 164 of the Incom...

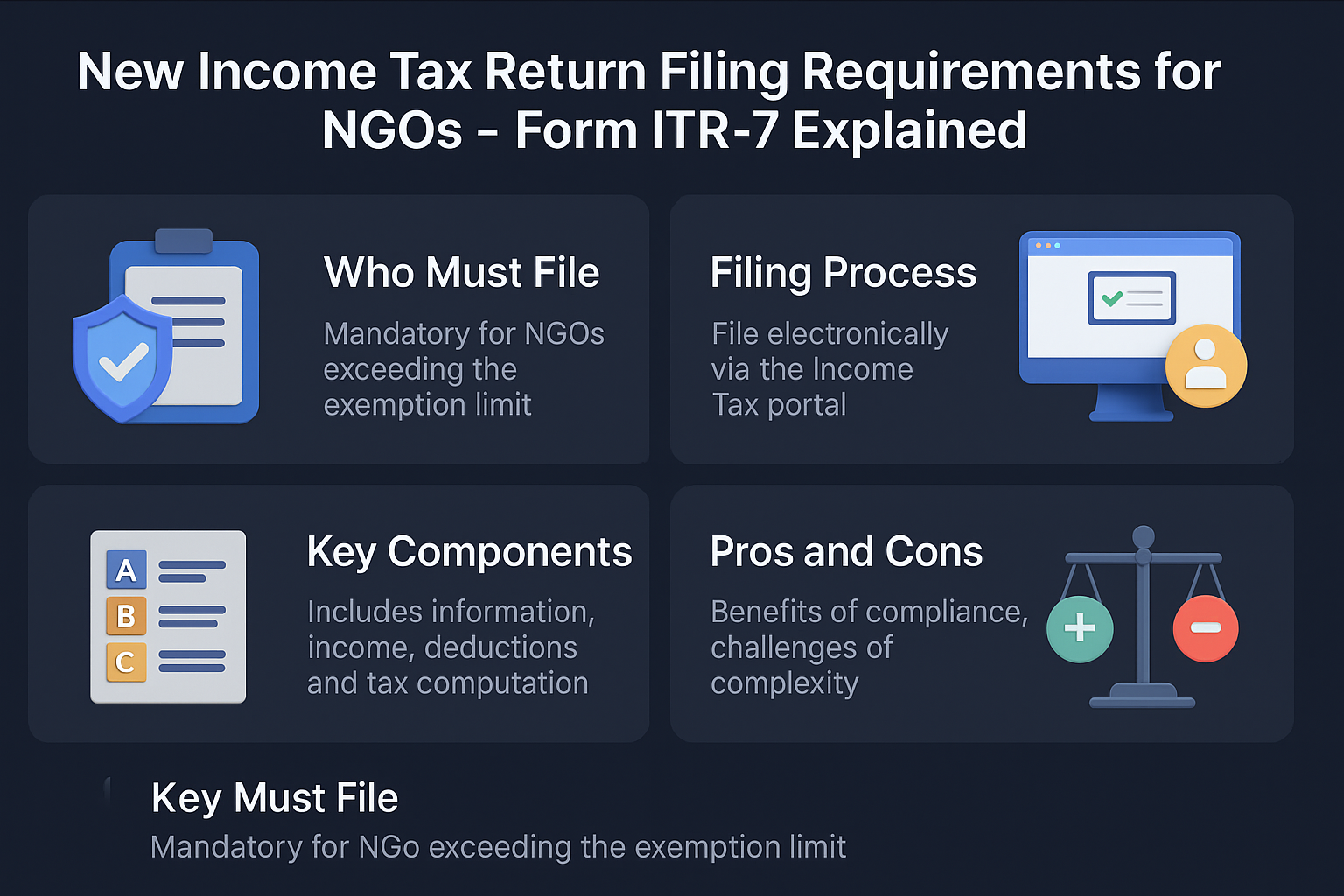

New Income Tax Return Filing Requirements for NGOs – Form ITR-7 Explained Legal Framewo...

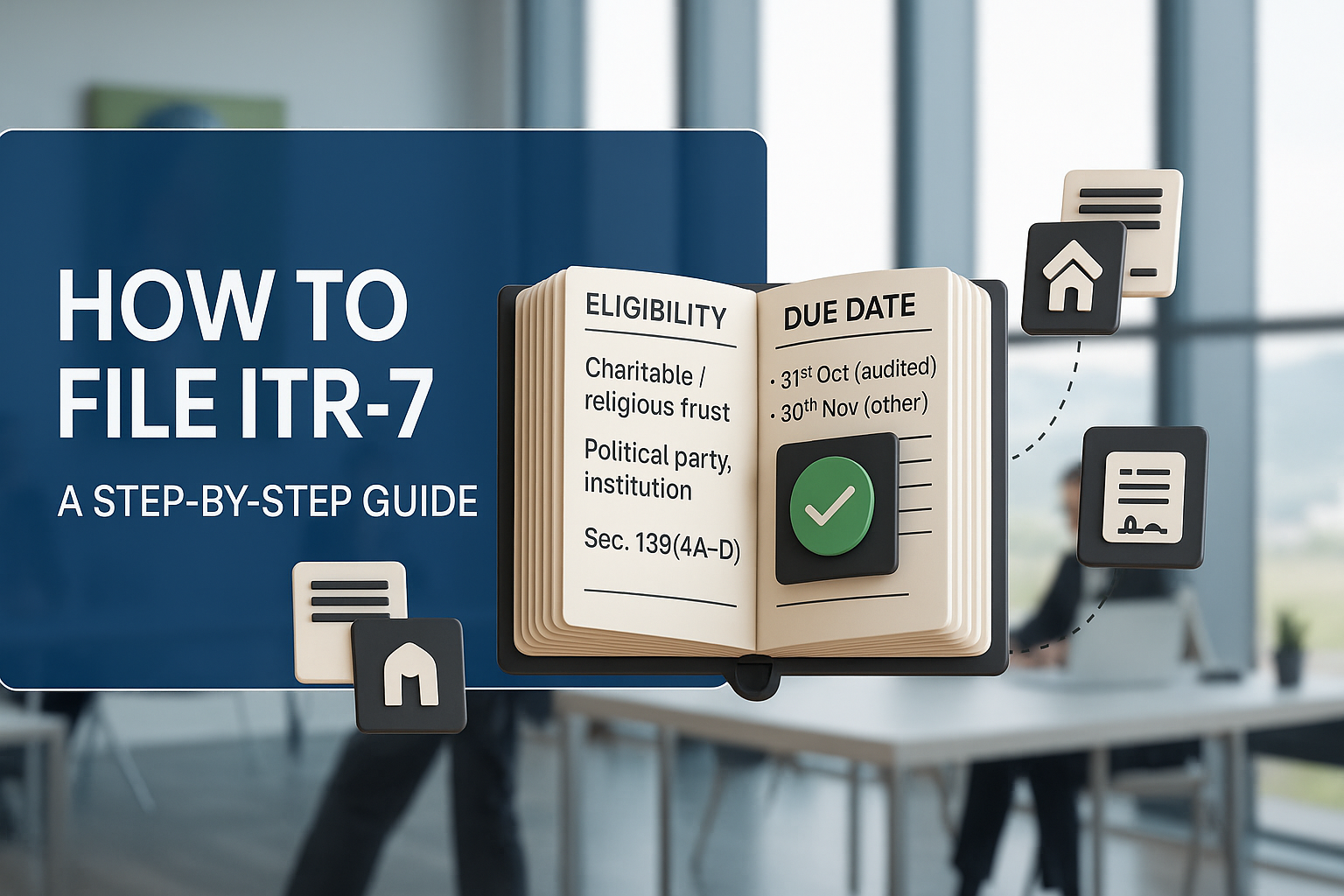

How to File ITR-7: A Step-by-Step Guide Who Must File. ITR-7 is the Income-tax return f...

How to File Annual Returns Under FCRA (Form FC-4) 3.1 Legal Framework Section 19 of t...

).png)

Understanding Societies in India: Formation, Governance, and Legal Framework Introduc...

)%20(2).jpg)

What is a REIT? A Real Estate Investment Trust (REIT) is a company that owns, manages, or ...

Private trusts and family trusts are like magical shields that protect your money and property. Th...

.png)

Impact of Mandatory Aadhaar Linking for NGO Trustees – Legal Validity & Privacy Concer...