).jpg)

Step-by-Step Guide to Registering a Charitable Trust in India

A charitable trust is a legal arrangement where one or more persons (trustees) hold and manage property for public charitable purposes. Under the Indian Trusts Act, 1882, a trust must be created for a lawful purpose and generally requires a written trust deed. In the case of immovable property, Section 5 mandates that the trust deed must be in writing and registered under the Registration Act, 1908. In practice, the registration of the deed (with the sub-registrar) and the trust’s name is carried out under state-specific laws, such as the respective State Charitable and Religious Trusts Acts, rather than through a centralized national system. Registration is essential as it grants the trust legal recognition and is a prerequisite for obtaining tax exemptions under provisions like Section 12A/12AB and Section 80G of the Income Tax Act, 1961.

Establishing a charitable trust requires drafting a proper trust deed and complying with all statutory formalities. The deed must clearly define the charitable objectives—such as education, healthcare, poverty relief, etc.—and must be registered, particularly when immovable property is involved. After the trust is created, it must apply for tax registrations under Sections 12A/12AB and 80G of the Income Tax Act to obtain exemption and deduction benefits.

Key Legal Provisions

1.1 Key Legal Provisions for Public Charitable Trusts in India

- Indian Trusts Act, 1882

- Section 4: Trusts must be for lawful purposes. “Lawful” means not fraudulent, not injurious to persons or property, and not opposed to public policy.

- Section 5: Trusts of immovable property must be created by a writing and registered under the Registration Act. Trusts of movable property likewise require writing unless the property is physically transferred.

- State Public/Charitable Trust Acts: Many states (e.g., Maharashtra, Tamil Nadu) have their own acts requiring registration of public trusts. Under these, registration is done with a Local Registrar of Public Trusts.

- Income Tax Act, 1961:

- Section 12A/12AA/12AB: Governs tax registration of trusts. Registration under Section 12A (provisional) or 12AB (current law) is needed for trust income to be tax-exempt.

- Section 80G: Allows donors to deduct donations if the trust has 80G approval.

Example –

Registration Requirement: Sita creates a public trust to run free clinics. Because her trust will hold land for a clinic, she drafts a trust deed, executes it on appropriate stamp paper, and registers it at the Sub-Registrar’s office (completing the requirement of Section 5 of the Trusts Act). She then approaches the Regional Assistant Charity Commissioner under the Maharashtra Public Trusts Act for a registration certificate.

1.2 Eligibility and Preparatory Steps

To register a charitable trust, ensure the following:

1.3 Drafting the Trust Deed

The trust deed is the founding document. It should include:

Important: The deed must not contravene law. For example, a trust cannot exclusively teach a religion and also get 80G (since pure religious propagation is excluded from “charitable” under IT rules).

1.4 Executing and Registering the Trust Deed

- Paying prescribed registration fee (e.g., ₹1100 in some states).

Presenting IDs (PAN/Aadhaar) of settlor and trustees.

- Possibly filling a short form with trust name, object, trustees details.

Upon acceptance, the Registrar issues a Certificate of Registration of the trust. This certificate is evidence of the trust’s formation but note that an unregistered trust deed (where registration is mandatory) is void.

1.5 Post-Registration Compliance

Once registered:

1.6 Timeline and Practical Steps

| Step | Description & Timeline |

| 1. Prepare documents | Draft trust deed (choose stamp paper; finalize trustees, objectives) – approx. 1 week. |

| 2. Trustee approvals | Convene trust board (or pass authorizing resolution) approving formation – 1 day. |

| 3. Registration | Submit deed at sub-registrar with fees and IDs – certificate issued in ~2–4 weeks (varies by state). |

| 4. Apply PAN/TAN | File online for trust’s PAN; apply for TAN if needed – PAN usually in ~1 week. |

| 5. Bank account | Open bank account once PAN & registration certificate are available. |

| 6. Tax registrations | File Form 10A (or 10AB if replacing provisional) on IT portal for 12A/80G – timeline: ~6–12 months including authority review. |

| 7. Commence activity | After legal formalities, start programs, while observing compliance (annual returns, 80G donation receipts, etc.). |

Example:

A newly formed trust in Delhi registers its deed on July 10. It obtains PAN by July 20 and opens a bank account by August. In September, it files online Form 10A for 12A and 80G. By November, it receives 12A and 80G certificates, valid for five years from the date of application.

The trust thus can accept tax-exempt donations.

1.7 Benefits and Pitfalls

Benefits of a charitable trust include simplicity of structure, low initial compliance, and direct control by trustees. They can be set up quickly and cheaply (low stamp duty and fees). Trusts can claim broad tax exemptions (if registered) and donors get 80G benefit.

Risks/Pitfalls:

No profit distribution: Like all NGO forms, surplus cannot go to trustees. However, unlike companies, trusts have fewer formal restrictions but also fewer formal checks (which can lead to governance issues if trustees are not diligent).

Trustee liability: Under the Trusts Act, trustees must exercise care and are liable for breach (Sec. 15 of Trusts Act). If trust funds are misused, trustees can be sued.

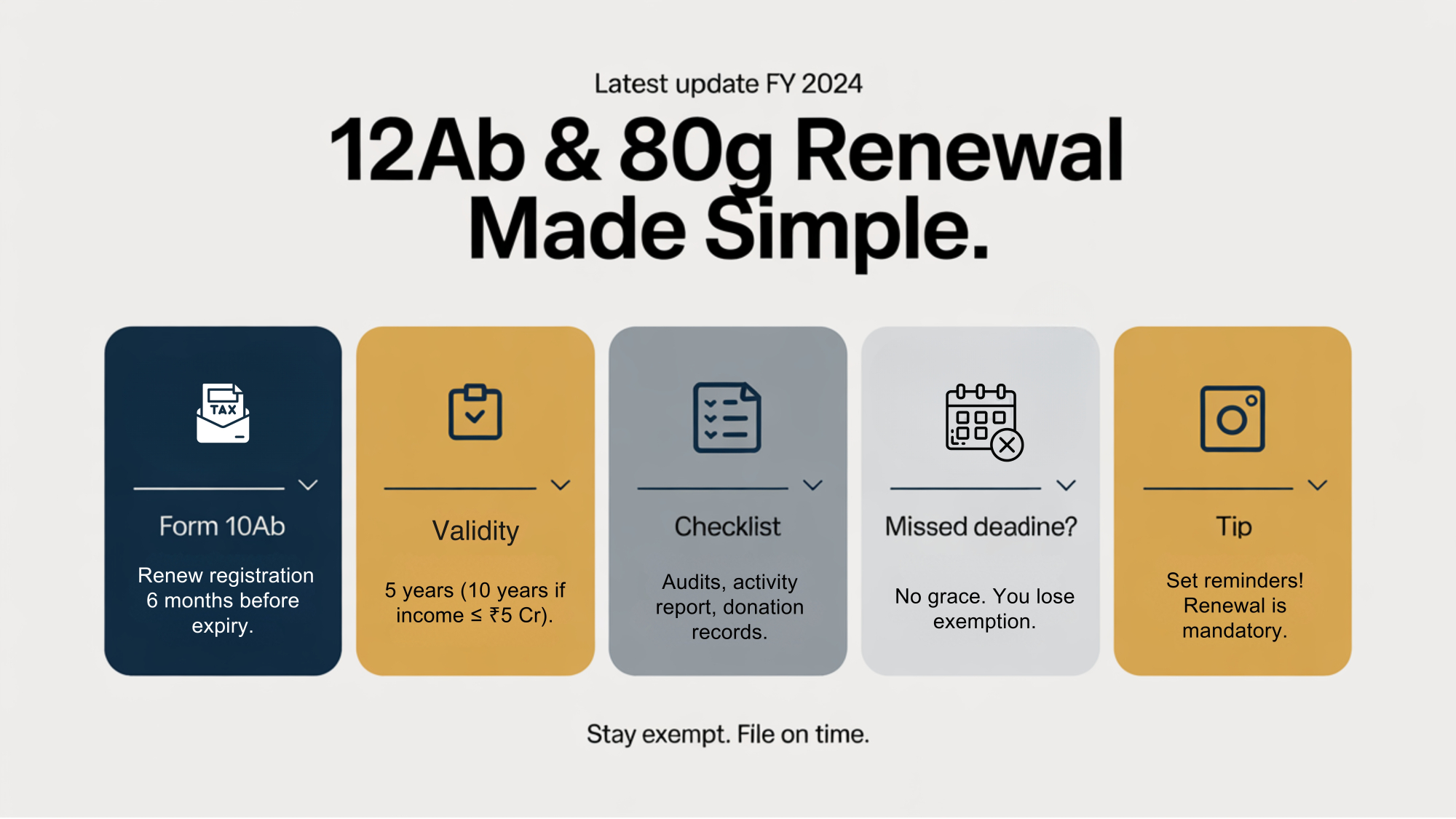

Compliance Tips: Keep detailed meeting minutes and accounts. Obtain a competent auditor’s annual audit even if not mandatory. Update the trust deed periodically to add trustees or amend objectives, but note major changes (like purpose or dissolving) may require court permission or following deed clauses. Ensure renewal filings (Form 10AB) are timely to avoid losing tax status.

“Registering a charitable trust establishes its legal foundation and enhances its operational capabilities through tax benefits and credibility.”

Understanding Charitable Trusts in India In India, the most commonly understood form of constitut...

)%20(1).jpg)

Understanding Religious Trusts Under Indian Law and Income Tax Act Religious trusts in India pla...

.jpg)

How to Apply for CSR Registration on MCA Portal Under Section 135 of the Companies Act and the C...

.png)

The rules and regulations that govern the functioning and operations of an Association of Persons ...

Private trusts and family trusts are like magical shields that protect your money and property. Th...

).jpg)

Government Grants: An Exhaustive Analysis Under Income Tax Law and Ind AS Framework Government...

Non-Profit Structures in India: Section 8 Companies, Trusts, Societies, and AOP/BOIs In India,...

Charitable Organisations – Taxation & Compliance (Legal Research Guide) Th...

Latest Rules for Renewal of 12AB & 80G Registrations Under current tax law, registe...

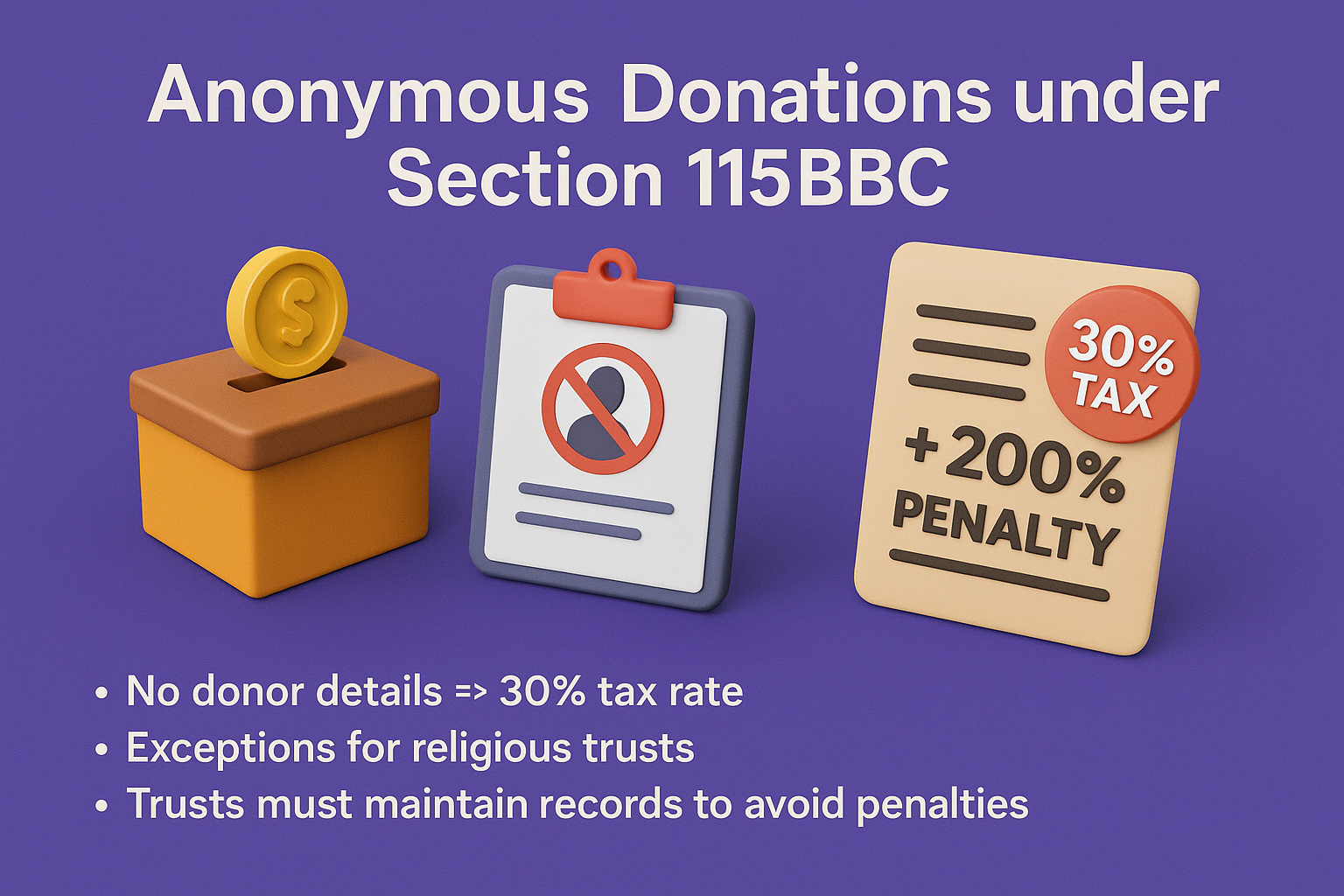

Anonymous Donations under Section 115BBC – Rules, Limits & Penalties Definiti...