Treatment of Foreign Services Online Courses,

Webinars by NGOs FCRA Risk

Overview

The proliferation of digital platforms has enabled NGOs to offer services like online courses and webinars to global audiences, generating income that supports their charitable missions. Under the FCRA, 2010, such income is generally excluded from the definition of foreign contribution if it represents payment for services rendered, but misclassification or non-compliance with FCRA protocols poses significant risks. NGOs must ensure that these earnings are not misconstrued as donations and are managed transparently to avoid penalties, suspension, or cancellation of registration. The inter play between FCRA and Income Tax regulations requires careful navigation to maintain compliance and leverage these income streams effectively.

Statutory Framework Section 2(1)(h)

Explanation 3 of the FCRA, 2010, explicitly excludes earnings from foreign sources for goods or services, such as fees for online courses or webinars, from the definition of foreign contribution. These are treated as commercial transactions, not voluntary donations, provided they are received in the ordinary course of business. However, Section 11 mandates that any funds classified as foreign contributions require FCRA registration or prior permission. The Income Tax Act, 1961, may treat such income as taxable under Section 28 if it exceeds the 20

Tax and Legal Treatment Analysis

Income from online courses or webinars provided to foreign clients is not considered a foreign contribution if it is a fee for service, such as a course on sustainable development offered to international participants. However, if the payment originates from a foreign donor with a pre-existing funding relationship, it may be scrutinized as a potential foreign contribution, requiring FCRA registration. NGOs without registration cannot accept such funds if they are deemed contributions, and even registered NGOs must deposit them in the SBI FCRA account if classified as such. Non compliance, such as accepting misclassified funds or failing to maintain separate accounts, can lead to penalties under Sections 3335, including fines, fund seizure, and imprisonment. Under the Income Tax Act, such income must be incidental to charitable objectives and within the 20.

Judicial and Regulatory Insights

The 2020 FCRA amendments clarified that service related income is distinct from foreign contributions, but the MHAs increased scrutiny of fund utilization, as seen in cases like Amnesty International Indias 2020 account freeze, underscores the risks of misclassification. The Supreme Courts 2022 ruling upholding FCRA amendments emphasized the need for transparency in all foreign transactions, including service income. The cancellation of over 20,000 FCRA registrations since 2011 for violations like financial irregularities highlights the MHAs rigorous enforcement, impacting NGOs offering online services.[](https://cof.org/news/new-indian-fcra-amendments impact-foreign-grants-indian-ngos)[](https://www.icj.org/resource/india-repressive-law-on foreign-contributions-stifles-ngos-must-be-revised-or-scrapped/)

Practical Scenarios

An FCRA-registered NGO offers an online course on environmental conservation to foreign participants, earning Rs. 5 lakhs, which is deposited in a commercial account as service income, exempt from FCRA. In contrast, an unregistered NGO accepts Rs. 3 lakhs for a webinar from a foreign donor, which is deemed a foreign contribution, leading to seizure and penalties. Another scenario involves an NGO receiv ing course fees from a foreign donor with a prior funding relationship, triggering MHA scrutiny and tax liability due to misclassification. A fourth case sees an NGO maintaining separate accounts for service income, ensuring compliance and avoiding FCRA risks.

Common Pitfalls and Mitigation Strategies

A common error is assuming all service-related income is exempt from FCRA without verifying the donors intent, risking misclassification as a foreign contribution. NGOs can mitigate this by clearly documenting the commercial nature of transactions. Accepting service fees in a non-FCRA account when they are deemed contributions invites penalties; using the SBI FCRA account for ambiguous transactions prevents this. Inadequate separation of service income from charitable funds can also lead to tax scrutiny; maintaining distinct accounts and audited records is essential. Engaging legal experts to classify transactions accurately reduces risks.

Professional Recommendations

NGOs should clearly document the commercial nature of online courses and webinars, specifying fees and services in contracts with foreign clients. Maintaining separate accounts for service income and ensuring it is not mixed with FCRA funds is critical. For registered NGOs, depositing ambiguous funds in the SBI FCRA account until classification is confirmed mitigates risks. Consulting legal and tax experts to assess the nature of transactions and conducting regular audits ensures compliance with FCRA and Income Tax regulations. NGOs should also monitor the 20

Conclusion

Income from online courses and webinars is generally excluded from FCRAs definition of foreign contribution, but misclassification or non-compliance poses significant risks. NGOs must ensure transparency, maintain separate accounts, and seek professional guidance to navigate these complexities. By adhering to FCRA and Income Tax regulations, NGOs can leverage digital services to support their missions while avoiding penalties and sustaining their legal standing.

Corpus Donations: Legal Definition & Practical Use What is a Corpus Donation? A c...

)%20(1)(1).png)

Is GST Registration Required for Section 8 Companies? With the introduction of the Goods and Ser...

Private trusts serve as powerful tools for asset management and wealth preservation, but understan...

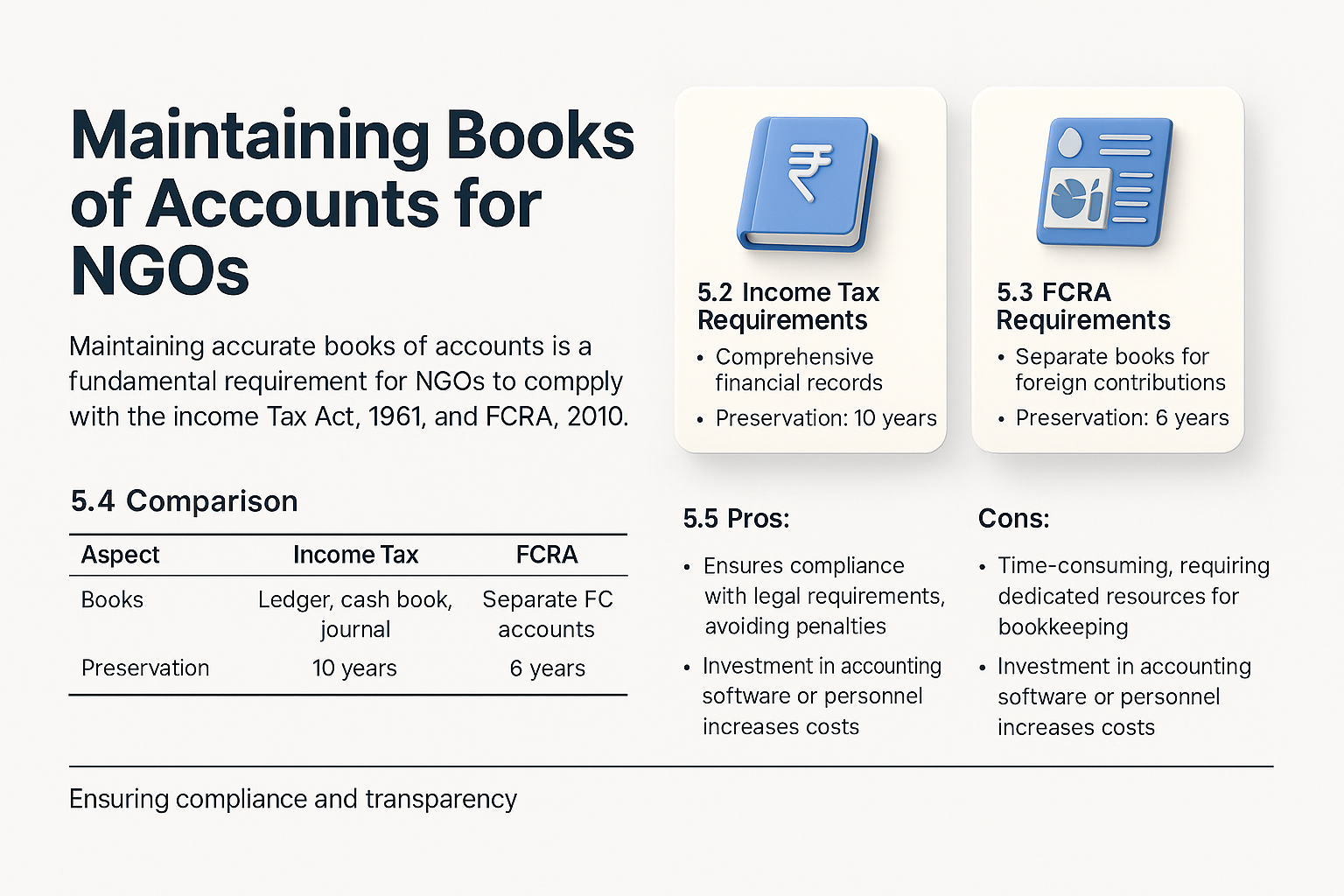

Maintaining Books of Accounts for NGOs Legal Framework Maintaining accurate books of ...

Foreign Travel for NGO Work: Does It Require FCRA Approval? The FCRA governs the acce...

FCRA Bank Account Designated vs Utilization Account Clarified Overview The FCRA, 2010...

).jpg)

Unregistered Trusts under the Income Tax Act, 1961 Legal Framework for Unregistered Trusts ...

).png)

Understanding Societies in India: Formation, Governance, and Legal Framework Introduc...

Tax Basics: The tax rules for private trusts are laid out in Sections 160 to 164 of the Incom...

.jpg)

How to Apply for CSR Registration on MCA Portal Under Section 135 of the Companies Act and the C...