)%20(1).jpg)

Understanding Religious Trusts Under Indian Law and Income Tax Act

Religious trusts in India play a significant role in preserving and promoting the country's diverse spiritual traditions. Rooted deeply in cultural and religious practices, these trusts are often established to support temples, rituals, spiritual teachings, and community welfare. While the Income Tax Act, 1961 does not explicitly define “religious trust,” various judicial interpretations and legal provisions provide a framework for their recognition and regulation. This blog explores the legal foundations, distinctions, tax implications, and modes of creation of religious trusts under Indian law, shedding light on how these entities function within both the religious and fiscal systems.

1. Definition and Scope of Religious Trust

The term 'religious trust' is not explicitly defined in the Income Tax Act, 1961. However, it is broadly understood as a trust established for the advancement, support, or propagation of religion and its tenets. The Supreme Court in Commissioner, "Hindu Religious Endowments v. Sri Lakshmindra Thirtha Swamiar of Shirur Math" (AIR 1954 SC 282) emphasized that religion is a matter of faith, and can include ethical rules, rituals,and modes of worship, regardless of whether they are theistic.

2. Distinction Between Charitable and Religious Trusts

While both types of trusts are eligible for tax exemption under section 11 of the Income Tax Act, key

distinctions exist:-

Charitable Purpose (Sec 2(15)): Defined explicitly in the Act.

Religious Purpose: Not defined, but generally involves promotion of religious doctrines and public worship.

It is worth noting that many trusts engage in both religious and charitable activities, forming what is known as Charitable and Religious Trusts

3. Public vs. Private Religious Trusts

Only public religious trusts qualify for tax exemptions under Section 11. Trusts set up exclusively for the

benefit of a particular family or private group are considered private religious trusts and do not enjoy tax

exemptions. Courts assess factors like public access to worship, public funding, and community rituals to

determine the nature of the trust

4. Essentials of a Valid Religious or Charitable Trust under Hindu Law

According to Hindu law and judicial precedents, four key elements are required:

1. A valid religious or charitable purpose

2. Capability of the author to create the trust

3. Clear identification of the trust property and purpose

4. The trust must not violate any law

No written instrument is necessary for religious endowments under Hindu law, although clear intent and

renunciation must be demonstrated

5. Religious Endowments

A religious endowment is the dedication of property for religious use, such as worship of a deity or

maintenance of religious places. These may be public (serving the community) or private (family-specific).Essentials include complete dedication, specific property, a clear purpose, and settlor's capacity.

6. Legal Provisions Under the Income Tax Act

Section 11 & 12 - Exemptions are available only to public religious trusts.

Section 10(23BBA) - Exempts income of statutory bodies managing public religious institutions.

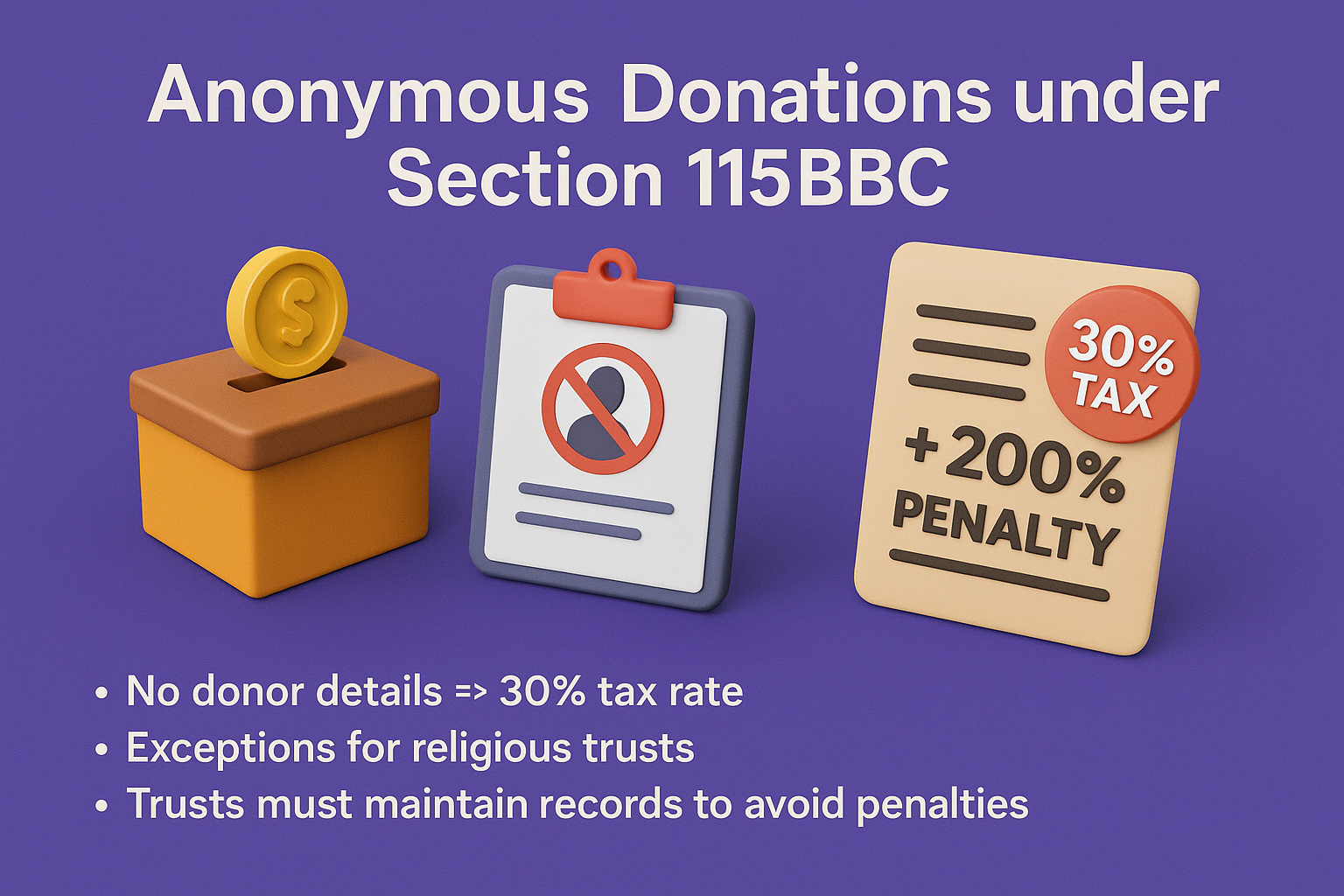

Section 115BBC - Anonymous donations to wholly religious trusts are not taxed

7. Modes of Creating a Religious Trust

Valid modes include:

1. Direct dedication to a deity

2. Gift to a trustee (under TPA, 1882)

3. Creation of a formal trust

No writing is required under Hindu law if the intention is clear.

8. Offerings and Donations

Offerings made to religious heads without linkage to a formal trust are not considered trust income. Donations to a registered religious trust, however, are eligible for exemptions under Section 12A

Conclusion

Religious trusts are a key part of India's spiritual and legal landscape. Their tax benefits and legal status

depend on clarity of purpose, public benefit, and adherence to statutory compliance under the Income Tax

Act

Tax Basics: The tax rules for private trusts are laid out in Sections 160 to 164 of the Incom...

).jpg)

Unregistered Trusts under the Income Tax Act, 1961 Legal Framework for Unregistered Trusts ...

Detailed Procedure for FCRA Registration and Renewal (Form FC-3A & FC-3C) Introdu...

).png)

Understanding Societies in India: Formation, Governance, and Legal Framework Introduc...

Introduction: Section 8 Companies, a distinctive provision under the Companies Act, 2013, embody ...

Non-Profit Structures in India: Section 8 Companies, Trusts, Societies, and AOP/BOIs In India,...

How to File Annual Returns Under FCRA (Form FC-4) 3.1 Legal Framework Section 19 of t...

Anonymous Donations under Section 115BBC – Rules, Limits & Penalties Definiti...

PUBLIC INSTITUTIONS EXEMPT FROM TAX [SECTION 10] The Income Tax Act of India, under S...

)%20(1)(1).png)

Is GST Registration Required for Section 8 Companies? With the introduction of the Goods and Ser...