Use of FCRA Funds for Asset Purchase

Overview

The FCRA, 2010, meticulously regulates the utilization of foreign contributions to ensure they align with the charitable objectives of NGOs and do not undermine national interests. The question of whether FCRA funds can be used for asset purchases is critical, as NGOs often require tangible assets like buildings, vehicles, or equipment to fulfill their missions. The Act permits such purchases under specific conditions, ensuring that assets directly support the NGOs registered objectives. However, stringent restrictions prohibit speculative investments or personal gains, and all transactions must comply with FCRAs banking protocols. Understanding these permitted and prohibited uses is essential for NGOs to maintain compliance and avoid severe penalties, including fund seizure and cancellation of registration.

Statutory Framework

Section 8 of the FCRA, 2010, mandates that foreign contributions be utilized solely for the purposes for which the NGO is registered, such as cultural, economic, educational, religious, or social programs. The FCRA Rules, 2011, further specify that assets purchased with foreign contributions must be acquired and held in the name of the NGO, as it is a separate legal entity. Rule 4 prohibits speculative investments, defined as activities with

a risk of appreciation or depreciation linked to market forces, such as mutual funds, chits, or land not directly tied to the NGOs objectives. Section 17 requires all foreign contributions to be received in a designated FCRA account at the State Bank of India (SBI), New Delhi Main Branch, with transfers to utilization accounts for expenditure, including asset purchases. Violations, such as misuse of funds, are punishable under Sections 3335, with penalties including fines, fund seizure, and imprisonment up to five years.

Permitted Uses

FCRA funds can be used to purchase assets that directly align with the NGOs registered objectives. For instance, an NGO focused on education may acquire land or construct a school building, while a healthcare-focused NGO might purchase medical equipment or a hospital facility. The key condition is that the asset must serve the charitable purpose for which the NGO is registered, and the Chief Functionary must undertake that these assets will be used exclusively for FCRA activities and not diverted for other purposes while the registration is valid. Assets must be owned by the NGO, ensuring they are not held for personal benefit. Additionally, the expenditure on such assets must not breach the 20.

Prohibited Uses

The FCRA imposes strict prohibitions on the use of foreign contributions for speculative investments or personal gains. Speculative investments include purchasing land or assets not directly linked to the NGOs objectives, such as buying property for resale or investing in mutual funds. Using FCRA funds for personal benefit, such as acquiring assets in the name of individuals, is strictly prohibited. Additionally, foreign contributions cannot be used for activities outside the NGOs registered purposes, such as funding political activities or projects unrelated to its mission. The 20

Legal and Tax Implications

Asset purchases with FCRA funds must comply with banking protocols, with all contributions received in the designated SBI account and transferred to utilization accounts for expenditure. Non-compliance, such as using funds for speculative purposes or failing to maintain proper ownership records, can lead to penalties, including seizure of assets under Section 25 and cancellation of FCRA registration. Under the Income Tax Act, 1961, such purchases are exempt under Section 11 if they align with charitable objectives, but mis use may render the funds taxable under Section 2(24). NGOs must maintain meticulous records to withstand MHA scrutiny and ensure tax exemptions.

Judicial and Regulatory Insights

The MHAs rigorous enforcement, evidenced by the cancellation of over 20,000 FCRA registrations since 2011, underscores the importance of adhering to permitted uses. Cases like the Centre for Policy Research (CPR), accused of using funds for undesirable purposes, highlight the MHAs scrutiny of fund utilization. The 2022 Supreme Court ruling upholding FCRA amendments emphasized transparency in fund usage, reinforcing the need for NGOs to align asset purchases with their objectives. Regulatory guidelines, such as those in the FCRA FAQs, clarify that assets must be held in the NGOs name and used for registered purposes.

Practical Scenarios

Consider an NGO registered for education that uses Rs. 20 lakhs of FCRA funds to purchase a building for a school, ensuring the asset is in the NGOs name and used for educational programs. This complies with FCRA and qualifies for tax exemption. In contrast, an NGO buying land for speculative resale with Rs. 10 lakhs of FCRA funds faces seizure and penalties for violating Rule 4. Another scenario involves an NGO purchasing medical equipment for a hospital but failing to document its use, leading to MHA scrutiny and potential tax liabilities. A compliant NGO transfers funds from the SBI Designated Account to a utilization account for a vehicle purchase, maintaining clear records to avoid issues.

Common Pitfalls and Mitigation Strategies

A frequent error is using FCRA funds for speculative investments, such as buying land for future profit, which violates Rule 4 and risks penalties. NGOs can mitigate this by ensuring all asset purchases directly support their objectives. Another pitfall is acquiring assets in individuals names, breaching the requirement for NGO ownership. Maintaining proper title deeds in the NGOs name prevents this. Inadequate documentation, such as failing to record asset usage, invites scrutiny; NGOs should maintain detailed records and conduct regular audits. Lastly, exceeding the 20

Professional Recommendations

NGOs should ensure that asset purchases align with their registered objectives, such as education or healthcare, and are documented as such. Acquiring assets in the NGOs name and maintaining clear title records is critical. All transactions must flow through the SBI Designated Account, with transfers to utilization accounts for expenditure. Engaging legal and financial experts to review asset purchase plans and conducting regular audits ensures compliance with FCRA and Income Tax regulations. NGOs should also stay updated on MHAguidelines to adapt to regulatory changes, ensuring that asset purchases do not jeopardize their registration.

Conclusion

FCRA funds can be used for asset purchases that directly support an NGOs charitable objectives, provided they are held in the NGOs name and comply with banking protocols. Prohibited uses, such as speculative investments or personal gains, invite severe penalties. By aligning purchases with their mission, maintaining transparency, and seeking professional guidance, NGOs can leverage FCRA funds effectively while avoiding legal repercussions.

High-Profile FCRA Cancellations and Key Lessons Overview The MHAs cancellation of ove...

How to Register Under DARPAN Portal and Its Relevance for NGO Grants Introduction The...

Anonymous Donations and Tax Liability Under Section 115BBC– What NGOs Must Know S...

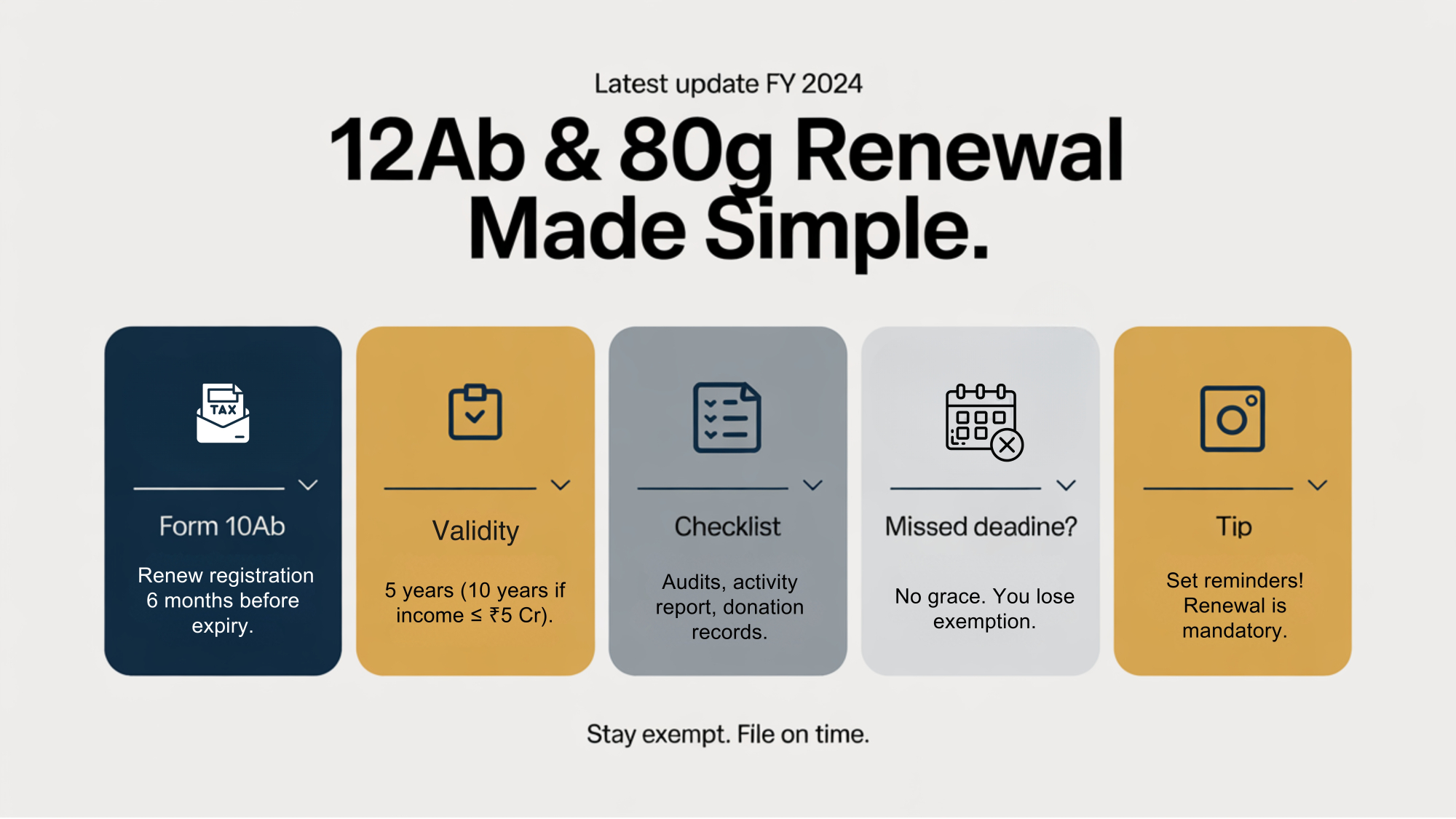

Latest Rules for Renewal of 12AB & 80G Registrations Under current tax law, registe...

)%20(2).jpg)

What is a REIT? A Real Estate Investment Trust (REIT) is a company that owns, manages, or ...

FCRA Renewal Process: Timeline, Documents, and Grounds for Rejection Overview The FCR...

A Complete Guide to Legal Structure, Registration, and Taxation of NPOs in India Introduction ...

FCRA Bank Account Designated vs Utilization Account Clarified Overview The FCRA, 2010...

How to Form a Section 8 Company: Procedure, Benefits & Pitfalls A Section 8 Company (Compa...

)%20(1).jpg)

What Is a Business Trust and How Does It Work? Definition There are several different types ...