What Constitutes “Charitable Purpose” Under Section 2(15)– Judicial Trends and Misinterpretations

Statutory Definition

Section 2(15) of the Income Tax Act, 1961, defines “charitable purpose” as including:

However, two provisos limit this definition:

These provisos aim to prevent misuse of tax exemptions by organizations engaging in commercial activities under the guise of charity

Historical Context and Amendments

The definition of “charitable purpose” has evolved to address concerns about tax evasion. Before 2008, the definition was broader, allowing organizations to engage in commercial activities if their primary object was charitable. The 2008 amendment introduced the first proviso to exclude trade or business activities unless incidental, while the 2010 amendment tightened this further by setting a 20% receipt threshold, replacing the earlier Rs. 25 lakh limit.

Judicial Interpretations

Judicial interpretations have shaped the application of Section 2(15), balancing public benefit with the prevention of commercial misuse. Key cases include:

Analysis of Judicial Trends

Courts have generally adopted a broad interpretation of “charitable purpose,” allowing activities that benefit the public at large. However, they scrutinize activities resembling trade or business, especially post-2008 amendments. The distinction between incidental and primary commercial activities is critical, with cases like Gujarat Cricket Association allowing incidental surpluses if reinvested, while Punjab Cricket Association denied exemptions for primary commercial motives.

Misinterpretations and Controversies

Practical Implications for NGOs

)%20(1).jpg)

Understanding Religious Trusts Under Indian Law and Income Tax Act Religious trusts in India pla...

Form 10BD and 80G Compliance Legal Framework Section 80G(5)(viii) of the Income Tax A...

.png)

The rules and regulations that govern the functioning and operations of an Association of Persons ...

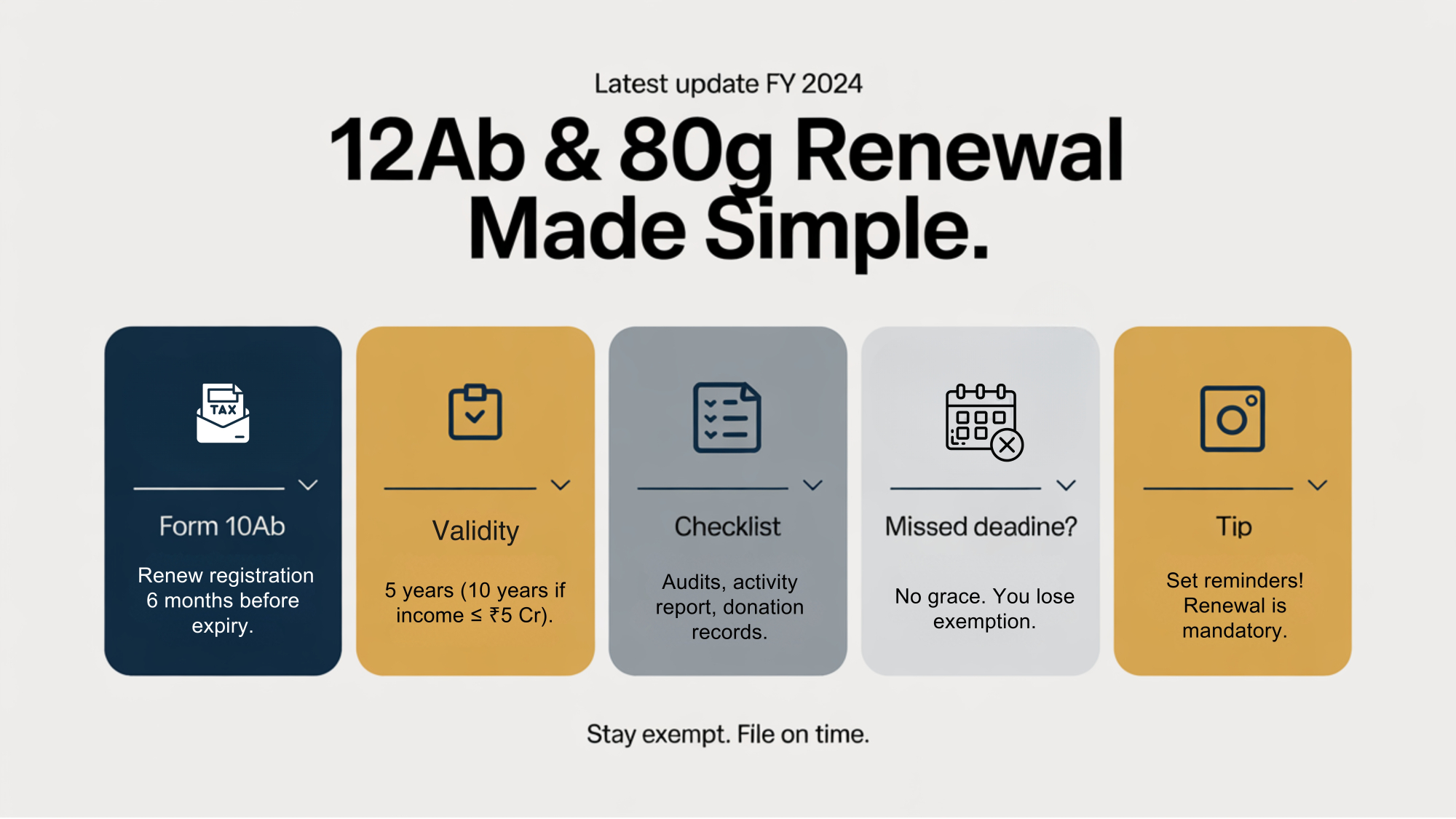

Latest Rules for Renewal of 12AB & 80G Registrations Under current tax law, registe...

Complete Guide to Form 10A and 10AB– New Compliance Framework for 12AB Registration &nbs...

Social Stock Exchanges 1.1 Background We often feel like helping t...

What is Form 10BB and How to File It – Audit Report for Charitable Institutions ...

).jpg)

Step-by-Step Guide to Registering a Charitable Trust in India A charitable trust is a legal arra...

.png)

BOI (Body of Individuals) and AOP (Association of Persons) are two different terms used in Indian ...

.png)

Impact of Mandatory Aadhaar Linking for NGO Trustees – Legal Validity & Privacy Concer...