Whether GST Should Apply to Donations Linked to Services– Controversy Around NGO Training In come

Introduction

The applicability of Goods and Services Tax (GST) to donations received by NGOs, particularly those associated with services like training or educational programs, is a contentious issue that has sparked significant debate in India’s nonprofit sector. The distinction between voluntary donations and payments for services—often referred to as quid pro quo arrangements—is central to determining GST liability, yet it remains mired in ambiguity. This section provides a comprehensive analysis of the legal provisions governing GST on NGO activities, the controversy surrounding training income, the implications for NGOs, relevant case laws, and proposed reforms to achieve clarity and equity in tax treatment.

Legal Provisions

The Central Goods and Services Tax (CGST) Act, 2017, and its associated rules form the backbone of India’s GST framework, with specific provisions relevant to NGOs:

Case Study: In *In re: Ecosan Services Foundation* (GST Authority for Advance Ruling, Maharashtra, 2020), services provided to an NGO for environmental preservation were deemed exempt if they aligned with charitable objectives. However, training programs with fees were held taxable, illustrating the fine line between charitable and commercial activities.

Controversy: Charitable vs. Commercial Activities

The core controversy revolves around the classification of donations linked to NGO services, particularly training programs, as either voluntary contributions or payments for services:

Example: “Skill India Trust,” an NGO registered under Section 12AA, conducts a six-month vocational training program for rural youth, charging 50,000 per participant as a “donation.” The trust argues that the program fulfills its charitable objective of skill development, but tax authorities classify the 50,000 as a service fee, imposing an 18% GST liability, which amounts to 9,000 per participant.

Relevant Case Laws

Judicial and quasi-judicial rulings have provided some clarity but also highlight inconsistencies:

Implications for NGOs

The application of GST to training income has far-reaching implications for NGOs:

A Comprehensive Guide to Social Audit in India In the modern era, citizens have become ...

Understanding the Concept of Corpus Fund – Treatment Under Income Tax & FCRA ...

Introduction: Section 8 Companies, a distinctive provision under the Companies Act, 2013, embody ...

.png)

EPF in India is a retirement savings scheme managed by EPFO under the Ministry of Labour and Empl...

PUBLIC INSTITUTIONS EXEMPT FROM TAX [SECTION 10] The Income Tax Act of India, under S...

Private trusts and family trusts are like magical shields that protect your money and property. Th...

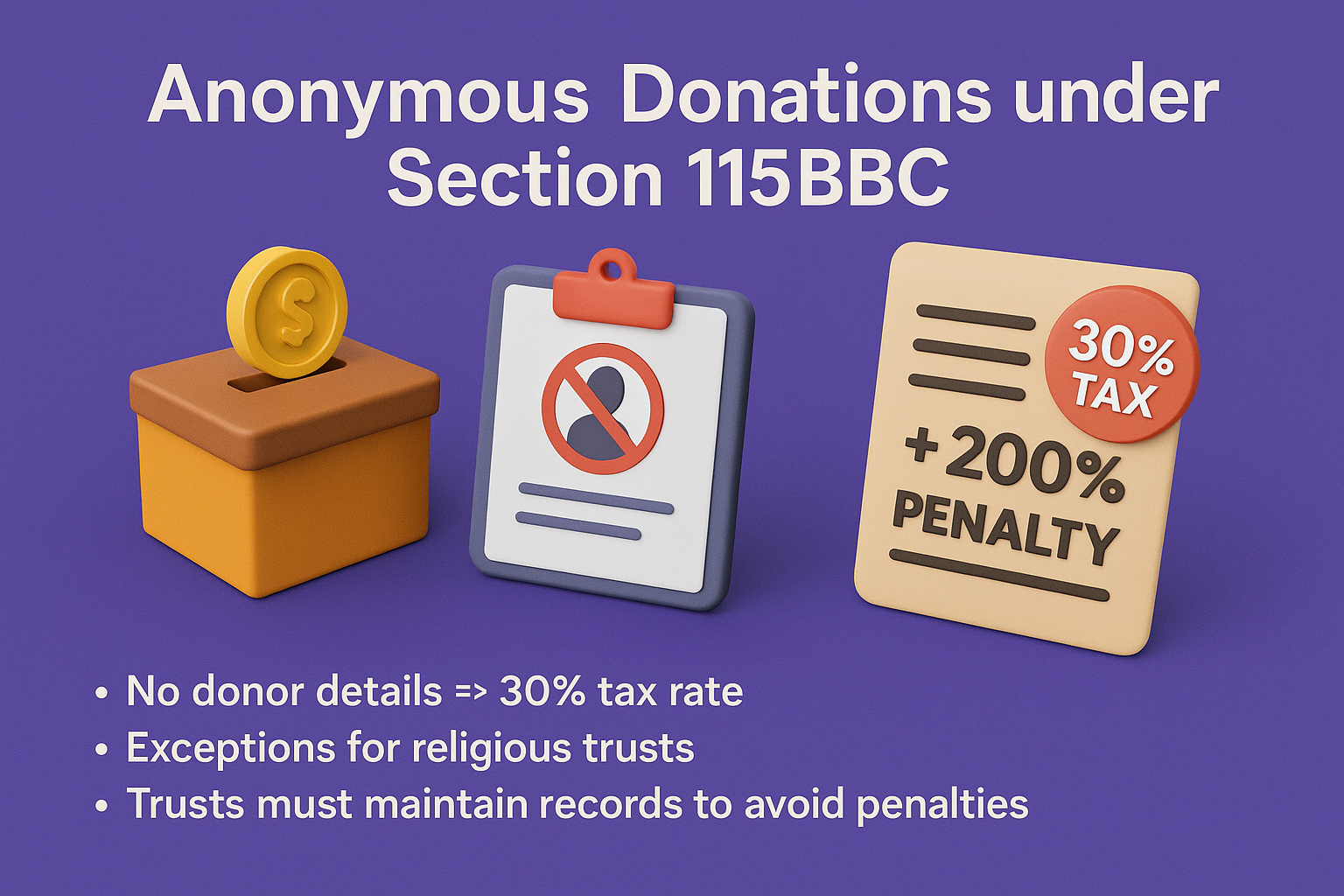

Anonymous Donations under Section 115BBC – Rules, Limits & Penalties Definiti...

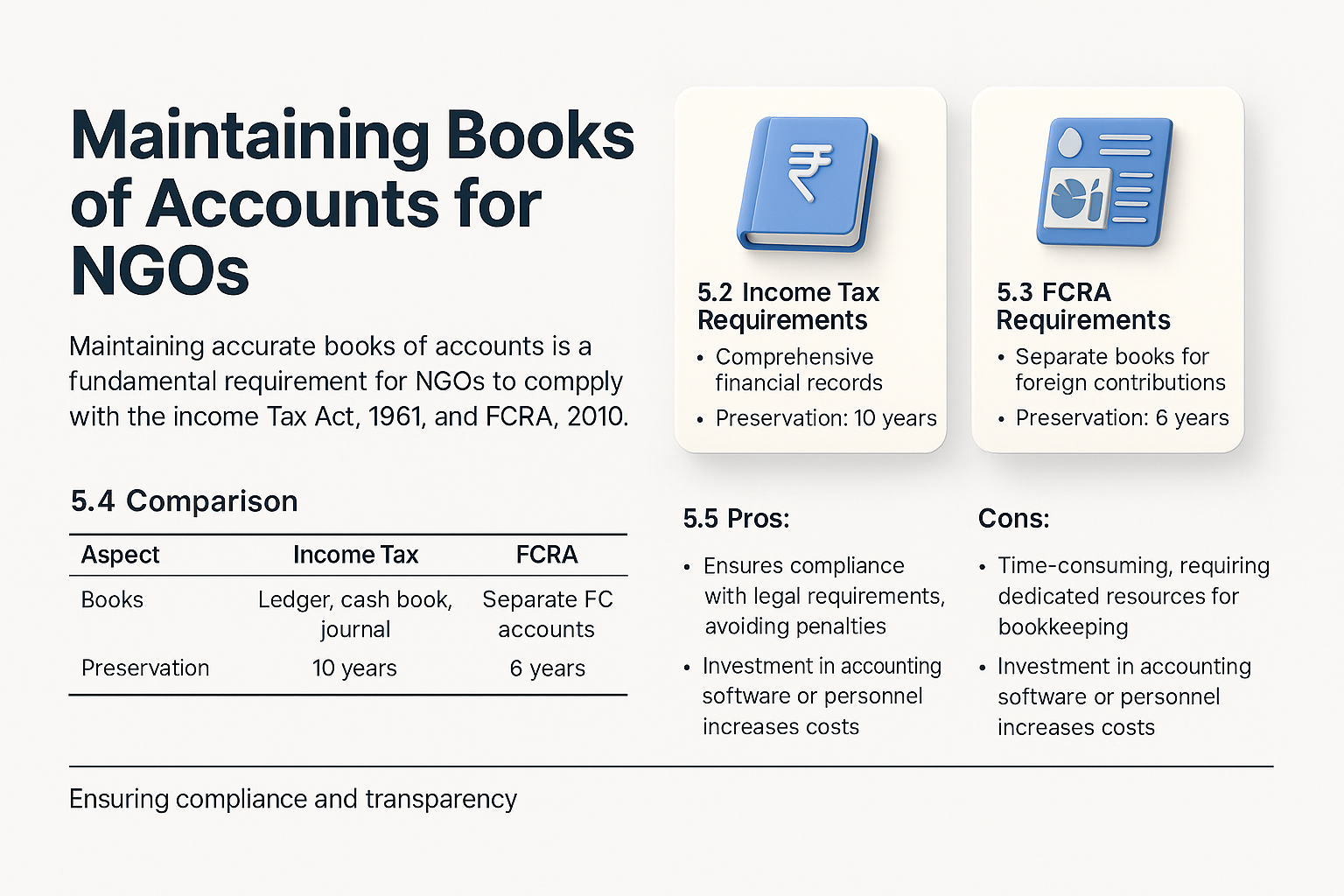

Maintaining Books of Accounts for NGOs Legal Framework Maintaining accurate books of ...

)%20(1)(1).png)

Is GST Registration Required for Section 8 Companies? With the introduction of the Goods and Ser...

.png)

The rules and regulations that govern the functioning and operations of an Association of Persons ...