INTRODUCTION

In today’s world, the trusts or institutions are being widely set up for the charitable purposes and imparting education among the poor. But lesser are known the facts about the taxability and registration of the trust or institution.

This newsletter is prepared to gives an insight of the trust with a broad and wide overview regarding the procedure of the registration and the exemptions available to a trust.

With a very strong foundation of cultural & moral values in India, every citizen tends or hope to help the ones in difficult time irrespective of one’s religion, caste, age, region etc. This divine light in heart and mind of every citizen in India always make us unique and different from rest of the World. Though one doesn’t need any specific institution to do anything good for another but by incorporating an institute a person can make sure that his/ her philanthropic work can be continued for an indefinite period.

One of the greatest examples is Tata Trusts which is one of the India’s oldest charitable organisations being set-up in 1892 by J N Tata Endowment. These trusts have played a very crucial role in pre-as well as post-Independent India’s philanthropic sphere. Its social works are spread in arts, charity, digital transformation, education, health, livelihood, nutrition, sanitation, social justice, sports, and skill development .

DEEDS SAMPLE

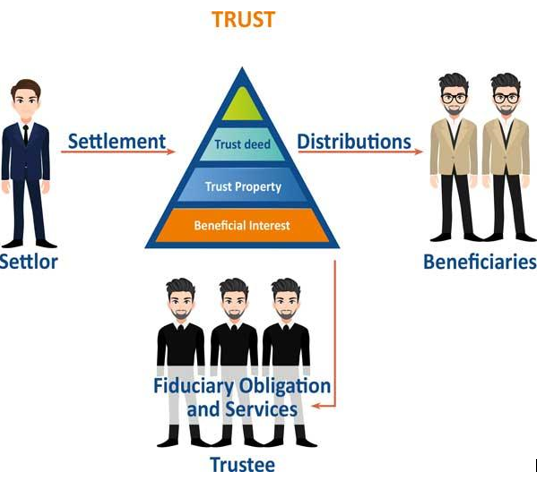

What Do You Mean By Trust?

Trust is defined in section 3 of the Indian Trust Act, 1882 as:

“An obligation annexed to the ownership of property and arising out of a confidence reposed in and accepted by the owner, or declared and accepted by him, for the benefit of another or of another and the owner”.

Simply said, it is a transfer of property by one person (settlor) to another (trustee) who manages that property for the benefit of someone else (beneficiary). The settlor must legally transfer ownership of the assets to the trustee of the trust.

Below is simplified chart

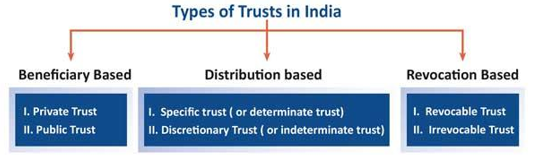

Types Of Trusts In India

There are basically two types of trusts in India: Private Trust and Public Trust. However they can be classified as follows:

While private trusts are governed by the Indian trusts Act, 1882, Public trusts are further classified into charitable and religious trusts. The Charitable and Religious Trust Act, 1920, the Religious Endowments Act, 1863, the Charitable Endowments Act, 1890, are some of the statutes for the enforcement of public trusts in India. Recently, trusts can also be used as a vehicle for investments, such as mutual funds and venture capital funds. These trusts are governed by Securities and Exchange Board of India (SEBI)

How The Creation Of Trusts Work In India?

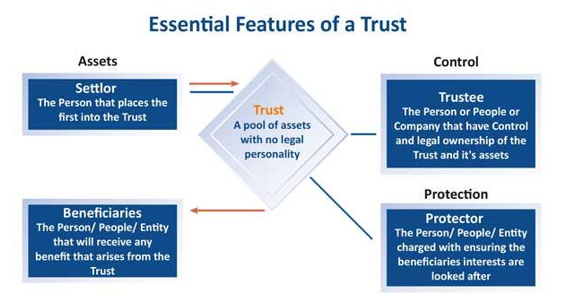

The following elements are essential for the formation of a Trust:

● An Author or Settlor of the Trust- the person who reposes or declares the confidence

● The Trustee – The person who accepts the confidence.

● The Beneficiary – The person for whom the confidence is reposed or declared.

● The Trust Property – It is the subject matter of the trust.

● The objects of the Trust – The intention of setting up of trust

Essential features of trust in india

As per Section 6 of The Indian Trusts Act, 1882 a Trust is created when the Author of the Trust indicates with reasonable certainty by any words or acts the following:

● An intention on his part to create a Trust;

● The purpose of the Trust;

● The Beneficiary; and

● The Trust Property, and unless the trust is declared by will or the author of the trust is himself to be a trustee transfers the Trust Property to the Trustee.

As per Section 4 of The Indian Trusts Act, 1882 a trust may be created for any lawful purpose. The purpose of a trust is lawful unless it is:

● forbidden by law, or

● is of such a nature that, if permitted, it would defeat the provisions of any law, or

● is fraudulent, or

● involves or implies injury to the person or property of another, or

● the Court regards it as immoral or opposed to public policy.

Every trust of which the purpose is unlawful is void. And where a trust is created for two purposes, of which one is lawful and the other unlawful, and the two purposes cannot be separated, the whole trust is void.

Further, if the condition mentioned above is satisfied then by executing a trust deed a trust can be formed. An oral trust is also valid but suffer from serious limitations.

A Trust deed is desirable and always advisable by experts to give trust a legal protection from becoming void anytime in future. When a private Trust pertains to an immovable property a written and executed trust deed is essential and shall also require to be registered except where the Trust is created by a will. In case of public Trust for immovable property, a written Trust deed is not mandatory but desirable. In relation to Trusts for movable property (public or private), a simple delivery of possession with a direction that the property be held under Trust, is sufficient; it requires no document or registration. It is however recommended that a formal trust deed is executed and registered to enable smooth functioning and recognition for all purposes.

Understanding Public Trust – Overview And Income Tax Implications

A trust is said to be a public trust when it is constituted wholly or mainly for the benefit of the public at large. Public trust are governed by the general law as the Indian Trust Act, 1882 is not applicable to public charitable trust. There is no specific act under which public trust can be established excepting in the state of Gujrat and Maharashtra

Public trust can be established for a number of purposes. In general, trust may register for one or more of the following purposes:-

● Relief to the poor

● Education

● Medical Relief

● Any other object of general public utility

Public trusts may be created inter vivos (transfer of property made during lifetime )or by will. Public trusts are further classified into charitable and religious trusts.

Before starting with details, the meaning of charitable purpose needs to be understood better which has been defined under Section 2(15) of the Income Tax Act, 1961 and stated as under: –

Charitable Purpose includes relief of the poor, education, yoga, medical relief, preservation of environment (including watersheds, forests and wildlife) and preservation of monuments or places or objects of artistic or historic interest, and the advancement of any other object of general public utility.

Provided that the advancement of any other object of general public utility shall not be a charitable purpose if it involves the carrying on of any activity in the nature of trade, commerce or business, or any activity of rendering any service in relation to any trade, commerce or business, for a cess or fee or any other consideration irrespective of the nature or use or application or retention of theincome from such activity unless :

The above section implies that if charitable activity is carried out for advancement of general public utility and during the course of such advancement if any activity in the nature of trade, commerce or business is carried out then such receipts should not exceed 20% of total receipts.

However, if the object of trust is relief of the poor, education, yoga, medical relief, preservation of environment (including watersheds, forests and wildlife) and preservation of monuments or places or objects of artistic or historic interest it will be regarded as a charitable activity regardless of incidental commercial activities.

Trust or institution when it is registered get a unique identity and various tax exemptions. If a trust wants itself to get the certificate for providing benefit of 80G to the donors in terms of the Income Tax Act, it shall first get itself registered under Section 12AA. The trust or institution may also get various government grants only when it is registered. Such registrations are required to be renewed by taking appropriate approval every 5 years. All existing Charitable trust are required to obtain a fresh registration on or before 31 August 2020

Conditions For Claiming Tax Benefit & Registration Of Trust

Section 12a – Conditions For Applicability Of Section 11 & 12

This Section provides that the provisions of Section 11 and 12 shall be applicable to a Trust or Institution only if the following conditions are satisfied: –

● The trust or institution has applied for registration to the Commissioner of Income Tax and is registered under Section

● Where subsequent modification has occurred in the objects which do not conform to the conditions of registration, the trust shall mandatorily apply to the Commissioner of Income Tax within a period of thirty days from the date of modification a fresh

● Where the Gross Receipts of the trust exceeds ₹2,50,000 in any previous year, then the accounts of the Trust or Institution shall be audited by a Chartered Accountant and such report shall be furnished within due date of filing of return for the relevant Assessment

The income tax return of the Trust or Institution has been filed within due date as prescribed in Section 139(4C) of the Act.

Section 12aa- Procedure For Registration

Dynamic Changes Introduced By Finance Act 2020 In Registration Process

The government has brought some major changes for Charitable Trust & Institution registered under Income Tax Act. Changes have been made in the area of obtaining registration and thereafter renewal of the same on periodical intervals.

The amendment state that “trust or an institution have to make application with the Principal Commissioner or Commissioner for registration of the trust as follows:

Trust already registered u/s 12A or section 12AA

Within three months from 01st October 2020 seeking for renewal of registration. The application will be disposed of within 3 months of date of receipt of application. The validity of the exemption granted is only for 5 years

Trust registered under section 12AB and the said period is about to expire

At least six months prior to the expiry of the said period.

Trust provisionally registered under section 12AB

At least six months prior to the expiry of the said period or within 6 months of commencements of activities whichever is earlier.

Registration becomes inoperative due to interplay of first proviso i.e. when such trust of institution is approved under section 10(23C) or notified under clause 10(46).

At least 6 months prior to the commencement of the assessment year from which the said registration is sought to be operative.

On modification of the objects of the trust which do not conform to the conditions of the registration.

Within a period of 30 days from the date of the said adoption or modification of the objects.

Understanding Private Trust – Overview And Income Tax Implications

"A trust is called a private trust when it is constituted for the benefit of one or more individual who are, or within a given time may be, definitely ascertained."

Private trusts are govern by Indian Trust Act, 1882.

The Basic features of private trusts are :

● Beneficiaries are limited and specified.

● Governed by Indian Trust Act,1882

● Beneficiaries are individual or As per Indian Trust Act 1886 “Every person capable of holding property may be a beneficiary.

A beneficiary is the person or persons who are entitled to the benefit of any trust arrangement. A beneficiary will normally be a natural person, but it is perfectly possible to have a LLP or company as the beneficiary of a trust. A proposed beneficiary may renounce his interest under the trust by disclaimer addressed to the trustee, or by setting up, with notice of the trust, a claim inconsistent therewith.

● Can be oral or written

Purpose Of Creation Of Private Trust ?

During the lifetime of the Settlor or Trust Creator:

- For the benefit of old parents,

- For the benefit of self, spouse, minor/major/disabled children/relatives,

- For protecting own interest,

- For the purpose of personal charity,

- To prevent alienation of personal/ancestral property.

After the death of the Settlor or Trust Creator:

- To safeguard the interest of spouse and children,

- To protect parents' old age commitments,

- For perpetual charity.

Who Can Create A Private Trust

A person can be settlor of a private trust if he has attained majority (i.e., has completed 18 years of age or in case of a minor, for whom a guardian is appointed by the court or of whose property the superintendence has been assumed by the court of wards the age of majority is 21 years) and is of sound mind, and is not disqualified by any law.

But a trust can also be created by or on behalf of a minor with the permission of a principal civil court of original jurisdiction. Apart from an individual, a company, firm, society or association of persons is also capable of creating a trust.

Who Can Be A Trustee

Every person capable of holding property may be trustee. Therefore even a minor can become a trustee. However, where the trust involves the exercise of discretion, he can accept or act as a trustee only if he is competent to contract.

No one is bound to accept trusteeship. Any number of persons of persons may be appointed as trustees as trustees.

Who Can Be A Beneficiary Of A Trust

Any person capable of holding property may be a beneficiary. Even unborn persons can be a beneficiary. The beneficiaries are one or more ascertainable persons.

How Long Can The Trust Operate

The trust will end at the time, or upon an event, specified in the trust deed. A trust cannot have infinite life.

Types Of Private Trust

● Revocable Trust – A trust that can be revoked (cancelled) by its settlor at any time during this life

● Irrevocable Trust – A trust will not come to an end until the term / purpose of the trust has been fulfilled.

●Discretionary Trust – An arrangement where the individual shares of the beneficiaries are not known, and the trustees decide the distribution of the income among the beneficiaries. In this case, Settlor lets the trustee decide which beneficiary gets which asset and in what The Settlor only decides beneficiaries. While the beneficiaries are identified, their beneficial interest in the Trust is not ascertained upfront.

● Determinate/ Specific Trusts: The entitlement of the beneficiaries is fixed by the settlor at the time of settlement or by way of a formula, the trustees having little or no discretion

Income Tax Implications of Private Trust

Taxation of a Specific Trust (Irrevocable):

- The beneficiaries and their shares are determinate and clearly stated in the trust.

- In cases where income does not include business income - Section 161(1):

- Tax is levied and recovered from the trustee as a representative assessee, similar to how it would be levied on and recovered from the beneficiary.

- Tax authorities can choose to assess beneficiaries directly, ensuring no double taxation occurs.

- Trustees can avail all benefits/deductions applicable to beneficiaries' shares of income, including tax slabs, exemptions, and deductions.

- No further tax is imposed on beneficiaries upon income distribution from the trust.

- Each beneficiary's applicable tax rate is determined and applied to trust income.

- In cases where income includes business income - Section 161(1A):

- The trust pays tax at 30% plus education cess and surcharge, equivalent to the Maximum Marginal Rate (MMR).

- MMR doesn't apply if the trust is created by will exclusively for the benefit of a dependent relative and is the sole trust declared by the settlor.

Taxation of a Discretionary Trust (Irrevocable):

- The shares of the true income owners (beneficiaries) are unknown.

- If trust income isn’t distributed among beneficiaries, the trustee pays tax in a representative capacity under Section 164(1).

- Tax recovery can occur from trustees or beneficiaries under certain conditions, avoiding double taxation.

- Tax treatment varies based on income and beneficiary circumstances:

- Income not including business income and specific conditions are met - Section 164(1):

- Taxable at individual slab rates for the Association of Persons (AOP) if beneficiaries' income is below the tax-free limit or specific trust conditions apply.

- Taxed at MMR otherwise.

- Income including business income - Proviso to Section 161(1A):

- Taxed at MMR.

Understanding these tax implications helps in managing trust finances and obligations efficiently while ensuring compliance with tax laws.

Tax Implications at the Time of Settling Property in a Trust by the Settlor: In the Hands of Settlor

- The property transferred to the trust by the settlor is not considered a transfer under Section 47(iii) provisions. This exemption applies to transfers of capital assets under a gift, will, or irrevocable trust, exempting them from capital gains tax. Therefore, no capital gains tax is applicable to the settlor when settling property under an irrevocable trust.

Section 47. Transactions not regarded as transfer:

- Clause (iii) exempts transfers of capital assets under a gift, will, or irrevocable trust from capital gains tax.

- If the trust is irrevocable, it falls squarely under the provisions of Section 47(iii), ensuring no capital gains arise for the settlor, and Section 50C of Income Tax is not applicable.

- Consequently, the recipient (beneficiary/trustee) inherits the cost of acquisition from the previous owner under Section 49(1), and the holding period includes the period the asset was held by the previous owner. This benefits the recipient in terms of tax calculations.

- If the settlor holds the asset as stock-in-trade, a business loss is booked. In such cases, the recipient doesn’t benefit from an extended holding period or the cost to the previous owner.

Taxability in the hands of the trustee on transfer of property

Section 56(2)(x) levies tax on receipt of property without consideration or for inadequate consideration. When a settlor settles a property on the trustee, there is an obligation on the trustee to use the property for the object of the trust and for the benefit of the beneficiaries.

Trustee receives the property which is held in a fiduciary capacity for the benefit of the beneficiaries. No gain, profit or rights accrue in the favour of the trustee in his personal capacity. In fact section 51 of the Indian Trust Act, 1882, clearly states that a trustee may not use or deal with the trust-property for his own profit or for any other purpose unconnected with the trust.

Hence, it cannot be said that Trustee acquires a right in rem or any beneficial right in the property which would be sine qua non for being taxed u/s 56(2)(x).

Hence, there will be no tax in the hands of the trustee(s).

Tax Implications at the Time of Settling Property by the Settlor in the Trust: In the Hands of Trust/Beneficiary

As per Section 56(2)(x), when money or property is transferred without consideration, it is chargeable under the head Income from Other Sources. The relevant extract of the Section is as follows:

- In the Case of Determinate Trust:

- The property is received by the trustee on behalf of and for the benefit of the beneficiary. Thus, the provisions of Section 56(2)(x) may be applicable.

- If the trust is created solely for the benefit of the settlor's relative, taxability will not arise due to the exception to Section 56(2)(x).

- In the Case of Indeterminate Trust:

- The beneficiary has nothing more than a hope that discretion would be exercised in their favor. In such cases, there is no taxability in the hands of the beneficiary.

- The provisions of Section 56(2)(x) may be invoked in the hands of the trust.

In any other case :

At least one month prior to the commencement of the previous year relevant to the assessment year from which the said approval is sought, and the said fund or trust or institution or university or other educational institution or hospital or other medical institution is approved under the second proviso

Moreover, it is pertinent to note that as provided in earlier before amendment only one-time registration under section 12AA shall be required but now the trust or institution has to, after every 5 years apply for mandatory renewal of registration under section 12AB.

Also as per the new proviso inserted in section 11 the trust can either claim an exemption under section 11 & 12 of the Act or under section 10(23C) of the Act. The trust has the discretion to choose only one of the exemptions.

Donation

The trust can apply for separate additional registration under section 80 G to enable the donations received by the trust to get a deduction to the Donor in respect of Donation given to the trust. This application can also be simultaneously be filed along with registration under Section 12AA/12AB.

Statement of donations

Every charitable trusts & specified institutions registered under the Section 80G of the Income Tax Act shall be required to file a statement of donations in the prescribed manner & deduction shall be available to donors based on information relating to donation furnished by such charitable trusts & specified institutions. The entities shall be liable to pay a penalty of INR 250 per day of delay in reporting to file a statement.

The deduction of cash donation under Section 80GGA of the Income Tax Act 1961 shall be restricted to INR 2,000 (earlier INR 10,000).

Taxation of Income of Trust

**Section 11(1) - Income from Property held for Charitable or Religious Purposes**

Incomes not included in the total income of the previous year:

- 15% of the Income derived from property held under trust, even if it is not spent and is accumulated.

- Income applied for purposes for which registration was granted.

- Income from voluntary contributions made with a specific direction to form part of the corpus of the trust or institution.

**Example:**

- Gross Receipts from properties held under trust for religious/charitable purposes: 20,00,000

- Voluntary Contributions (donations) received from donors: 2,00,000

- Voluntary Contributions received with a specific direction to form part of the corpus of the trust: 3,00,000

- Expenditure on activities of religious or charitable nature: 4,00,000

**Solution:**

1. Gross Receipts from properties held under trust for religious/charitable purposes: 20,00,000

2. Add: Voluntary Contributions received: 2,00,000

Total: 22,00,000

3. Less: 15% Accumulation (15% of 22,00,000): 3,30,000

Net Income: 18,70,000

4. Less: Expenditure on activities of religious or charitable nature: 4,00,000

**Total Income: 14,70,000**

image - 4

Points To Be Noted

● The trust shall be liable to obtain a PAN only if

● If the total income exceeds maximum amount which is not chargeable to tax.

● A charitable trust who is required to furnish return under Section 139(4A)

● Every person who intends to enter into specified financial transactions in which quoting of PAN is mandatory

Even though the trust is not covered in any of the above criteria we suggest that Trust shall apply for PAN voluntary. Further Trust should also obtain a TAN considering its future activities and tax compliances.

● For a trust to be eligible for making an application to obtain a FCRA certificate following criteria should be satisfied:

1. The trust should be registered under the Indian Trusts Act, 1882 or under Section 8 (erstwhile Section 25) of the Companies Act, 2013;

2. The trust should be in existence for at least 3 years and has undertaken reasonable activity in its chosen field for the benefit of the society for which the foreign contribution is proposed to be utilized.

3. The trust should have spent at least 10,00,000/- over the last 3 years on its aims and objects, excluding administrative expenditure.

4. Statements of Income & Expenditure, duly audited by CA, for the last 3 years are to be submitted to substantiate that it meets the financial parameter.

● If in any previous year, the charitable or religious trust fails to apply its 85% of its total receipts towards the objects then such shortfall of receipts shall be taxable in the hands of the However if :

● The reason for non-application of the receipt of income is that the whole or any part of the income has not been received during that year or

● The amount has been accumulated or set apart for application for specified such purposes in India in the future.

Then such receipt shall deemed to have being applied for the purpose of Sec-11. However for receipt mentioned in former point-1 (a) shall have to be applied in the year in which it is actually received. Further for claiming any amount as set-apart in terms of 1 (b), a prescribed form has to be furnished to the concerned officer within the due date of filing the return.

● Also, the trust or the institution has an option to accumulate or set apart, either in whole or in part, for application to such purposes in India, such income so accumulated or set apart shall not be included in the total income of the previous year of the person in receipt of the income, provided the following conditions are complied with namely: –

● The trust shall file a Form 10 with the Assessing Officer specifying the purpose and period (which in no case shall exceed 5 years) within the due date specified under Section 139(1).

● The money so accumulated or set apart should be invested in the modes specified under Section 11(5).

● The Income tax return of the trust or institution is furnished within due date mentioned under Section 139.

● Anonymous donations are donations which taxpayers make to a place or person where proper records are not maintained. Exemptions are allowed up to 5% of the total donations or Rs.1,00,000, whichever is higher, rest are taxed at the rate of 30%. However, donations offered to a trust which is entirely religious in nature will be provided with a complete exemption. If the anonymous donation is received for educational purposes, and the Trust operates the same, such donations would be taxable.

● Further, as per the provisioning of Section 11(7), where a trust or an institution has been granted registration under Section 12AA and the said registration is in force for any previous year, then the trust cannot claim any exemption under any provision of Section 10 except under Section 10(1) and Section 10(23C).

● Furthermore, the provisions of Section 40(a)(ia) [dis-allowance on account of non deduction of TDS] and Section 40A(3) [disallowance of expenditure incurred in cash exceeding INR 10,000 per person in a day] and Section 40(3A) [dis-allowance of payment made to the outstanding Liability in cash exceeding INR 10,000 per cash] shall mutatis mutandis apply as they apply in computing the income chargeable under the head “Profit and gains of business and profession”.

● The tax rates applicable to the trust are the same as that to an individual.

Incorporation of a trust

There must be at least two or more persons for forming the trusts. The trust must be formed according to the provisions of the Indian Trusts Act, 1882. The parties must not be disqualified under any law in force in India. The objectives of the trust must not go against any law in force in India.

The process for Trust Registration begins with the registration of the Trust Deed. After the deed is drafted, it is submitted to the Office of the Registrar of Trust with the documents of the settlor, and the witnesses. These documents would include their photographs, identity, and address proofs.

Documents required for trust registration

Complete process of trust registration

image - 5

Taxation on trust

For the purpose of long-term capital gains, the holding period should be more than 36 months. Short term capital gains shall be taxable @30% for residents and 40% for non-resident corporates. The other income of the business trust shall be taxable at the Maximum Marginal Rate @42.7%.

Charitable/religious trusts are the trusts which are formed with an objective of providing relief to poor, education, medical relief, preservation of objects of general public utility, religious purpose, etc. There taxation has always been a point of concern. The entire income of such trust (be it house property, capital gain or any other income) is taxed as per the provisions of section 11-13 of income tax act, 1961 rather than as per their relevant provisions.

Understanding Charitable Trusts in India In India, the most commonly understood form of constitut...

.png)

EPF in India is a retirement savings scheme managed by EPFO under the Ministry of Labour and Empl...

Tax Basics: The tax rules for private trusts are laid out in Sections 160 to 164 of the Incom...

Private trusts serve as powerful tools for asset management and wealth preservation, but understan...

Private trusts and family trusts are like magical shields that protect your money and property. Th...

NPOs should develop an action plan to address audit findings, assign responsibilities, and implement corrective actions. Open communication with auditors and a commitment to continuous improvement are essential.