List Of Sections

| Section 11 | Trust eligible for exemption |

| Section 11(1) | Income from property held under trust for charitable and religious purposes |

| Section 11(1)(a) | Trust created wholly for charitable or religious purposes and applying (or accumulating) their income to such purposes in India |

| Section 11(1)(b) | Income from property held under Trust which is applied in Part only for Charitable or Religious Purposes |

| Section 11(1)(c ) | Income from Property held under Trust which is applied for Charitable purposes outside India |

| Section 11(1)(d) | Voluntary contribution forming part of corpus |

| Section 11(1A) | Tax treatment of capital gain from property held under trust |

| Section 11(1B) | Consequences if the income is not actually applied within the prescribed period after exercising the option |

| Section 11(2) | Accumulation of income in excess of 15% of the income earned |

| Section 11(3) | Withdrawal of Exemption granted to income accumulated under section 11(2) |

| Section 11(3A) | Circumstances where the accumulated income in excess of 15% can be utilized for a purpose other than that for which it was accumulated |

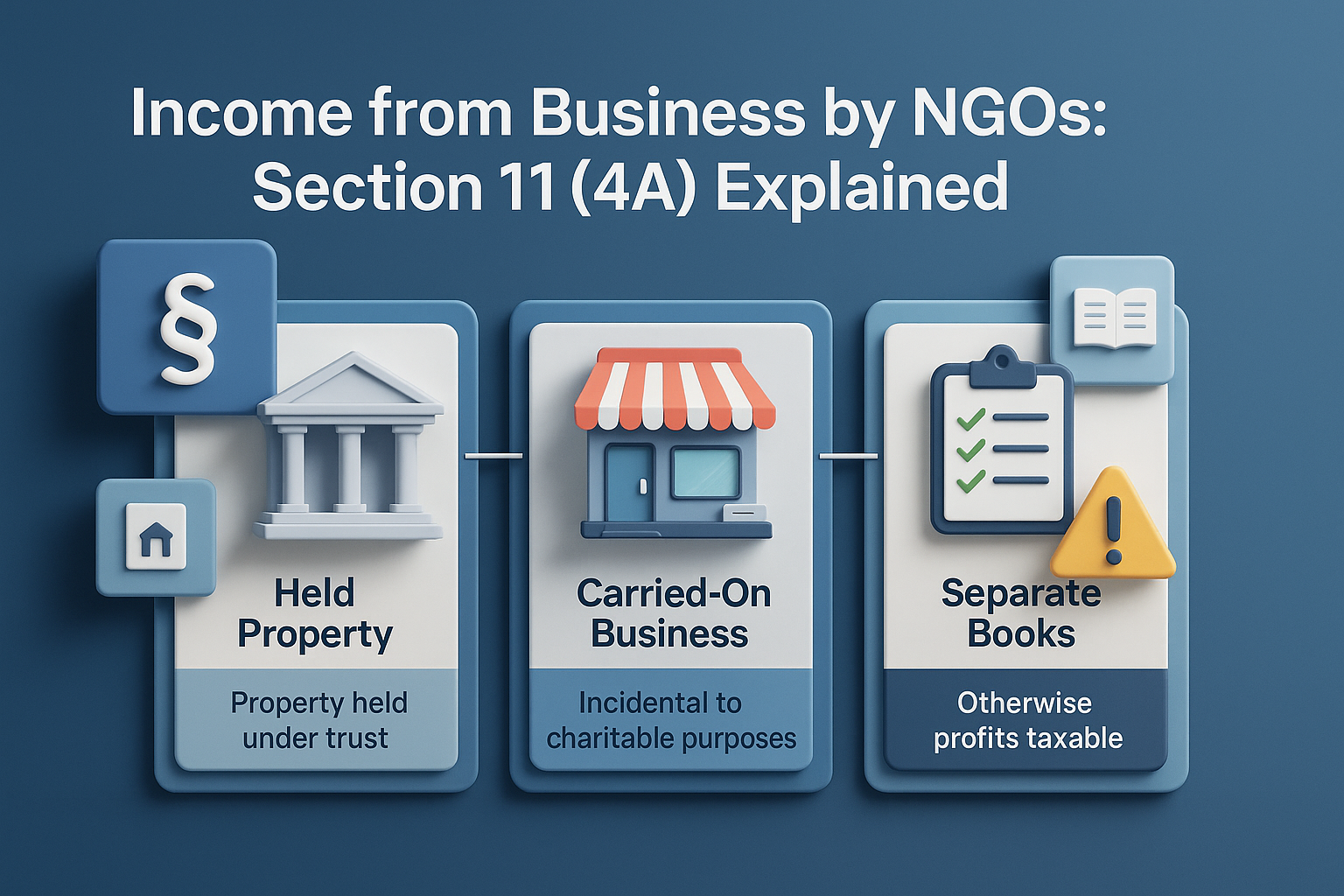

| Section 11(4) | Income from a business carried on by the trust |

| Section 11(4A) | Profits and Gains from Incidental Business |

| Section 11(5) | Modes of investment or deposits by a Charitable or Religious Trust or Institution |

| Section 11(6) | For the purposes of accumulation or setting apart of income for application, depreciation on assets, the acquisition of which have been claimed as application shall not be allowed |

| Section 11(7) | Assessee can either obtain registration under section 12AB or obtain approval under section 10(23C), but cannot adopt both |

| Section 12(1) | Voluntary or contributions (Donation) not forming part of corpus of the Trust or Institution treated as income |

| Section 12(2) | Value of medical/education services provided to specified persons by trust running Hospitals and educational institution – Exemption under section 11 shall not be available for services provided to specified persons |

| Section 12A | Conditions for applicability of Sections 11 and 12 |

|

Section 12AA(3) & 12AA(4) |

Cancellation of Registration of the Trust or Institution |

| Section 12AB | Procedure of registration of a Trust/Institution |

| Section 12AB(4) | Cancellation of Registration or provisional registration of a trust or an institution under certain circumstances |

| Section 13(1) | Forfeiture of exemption to Trust and Institutions |

| Section 13(2) | Income for the benefit of a person specified in section 13(3) |

| Section 13(3) | Meaning of specified persons (as referred to in clause (c) of sub-section (1) and sub-section (2) of Section 13) |

| Section 13(4) | Exemption not be denied if the investment of the trust or institution in which the specified person has a substantial interest |

| Section 13(5) | Exemption under sections 11 and 12 shall not be denied if Debentures purchased after 28.02.1983 but before 25.07.1991 do not continue to remain invested beyond 31.03.1992 |

| Section 13(6) | Charitable trusts not lose exemption if educational or medical facilities provided to specified persons |

| Section 13(7) | Anonymous Donation specified in section 11BBC not exempt |

| Section 13(8) | When commercial receipts exceeds the specified threshold |

| Section 13(9) | In case return is not filed by prescribed date then benefit of accumulation under section 11(2) will not be available |

| Section 13(10) | Section 13(8) is applicable to any Trust or where the Trust violates the provisions of Section 12A(1)(b)/(ba), income chargeable to tax will be for expenditure incurred for its objects, subjects to certain conditions |

| Section 80G | Procedure for Registration for Exemption Certificate |

| Section 115BBC | Anonymous donations to be taxed in certain cases |

| Section 115BBI | Specified Income of Certain Institutions |

|

Section 115TD, 115TE & 115TF |

Special provisions relating to tax on accreted income of certain Trusts and Institutions |

Introduction: Section 11

Section 11 of the income Tax Act 1961, which is a charging section, is applicable to charitable or religious institutions, provides exemption on the application of income. The language provides that the exemption would apply when the income derived from the property held under trust is applied or is deemed to have been applied for charitable or religious purposes.

Parts of section 11

1. The income must be derived from the property held under trust or legal obligation.

2. Such trusts or other legal obligation should be wholly for religious or charitable purposes.

3. Such income is applied or accumulated for application to such religious or charitable purposes within the taxable territories of India.

4. To the extent to which the income so accumulated or set apart is not in excess of 15% of the income from such property.

Section 11 of the Income Tax Act 1961, uses the expression ‘such income’ in section 11(1).

It includes all income which is derived from the property held under trust and includes the income which is deemed as income derived from property held under trust. For example, the voluntary contributions are deemed as income derived from property held under trust and treated as income under section 224)(iia) of Income Tax Act 1961

Meaning of such income

1. Income from the activities of the trust

2. Interest income

3. Dividend income

4. Voluntary contribution

5. Income from the property

6. Capital gains on sale of property

7. Income derived from the investments.

Such purposes in India

The most important part of section 11(1) is ‘such purposes’.

Meaning of such purposes are following:

1. It means the charitable or religious purposes.

2. It means the purposes which are traversed in the constitution.

3. It means the objects which are mentioned in the instrument.

4. It means the purposes which are constituted and which are notified at the time of seeking registration.

The occurring of the expression, ‘Such purposes in India’ has a special significance. In order to claim exemption applying income for such purposes in India is a pre-requisite condition.

In this regard, the issue which arises for consideration is as follows:

1. Whether the application should be in India?

2. Weather such proposes in India includes amount applied outside India for the objects in India?

Application in India

The first view is that for the purposes of claiming exemption the application of income has to be made in India. The application, in other words, means the amount has to be spent in India. If the amount is applied outside India, it does not satisfy the condition as required under Section 11 of the Income Tax Act 1961.

Application outside India, purposes in India

The second possible view is that the application made outside India but for the purposes in India, therefor, there is no infringement of section 11(1) of the Income Tax Act 1961. However, if the application and purpose is outside India a permission from the CBDT has required.

Hypothetical income: In the case of CIT v/s Shoorji Vallabh Das & Co. (1962) 46 ITR 144 (SC). The income to be received in real sense in hand of the trust.

Head wise computation not applicable: In the case of CIT v/s Rao Bahadur Calavala Cunnan ITR 12(Mad), it was held that the income has to be arrived in the normal commercial manner without applying section14.

Example:-

Rent income received from the house property cannot be computed under section 22.

Section 11(1)(a)

Section 11 income from property held for charitable or religious purposes

Section 11(1) subject to the provisions of sections 60 to 63. The following income shall not be included in the total income of the previous year of the person in receipt of the income-

(a) Income derived from property held under trust or institutions wholly for charitable or religious purposes to the extent that such income is applied to charitable and religious purposes in India, and where any income is accumulated or set apart for application to such purposes in India, to the extent to which the income so accumulated or set apart is not in excess of 15% of the income from such property.

Meaning of applied- The word applied has been used in a broadest sense this term upholds all expenditures whether revenue or capital incurred for the purposes of charitable or religious.

1. It recognizes not only the amount spent but also earmarked for future spending. This is evident from reading of section 11(2) of the income tax act, 1961.

2. It consists of all expenditures incurred irrespective of revenue or capital in nature.

3. Deemed application is an ‘application’. This is apparent from reading of section 11(2) of the income tax act, 1961.

4. Mere passing book entry without earmarking of funds could not be said to ‘be applied’.

Examples of the application of income:

1. Establishment expenses

2. Administrative expenses

3. Capital expenditure

4. Payment of taxes

5. Repayment of debts

6. Salary paid to trustees and managers

7. Inter charity voluntary donation from the current year income

Section 11(2) Accumulation of income

[Section 11(2)] : Accumulation or Setting apart of the Trust Income for a Specific Purpose

Accumulation of income in excess of 15% of the income earned [Section 11(2)]

As already mentioned, assessee is allowed to accumulate upto 15% of the income earned during the year for application for charitable or religious purposes in India in future. If the assessee wants to accumulate or set apart the income in addition to 15% of the income, he can do so if certain conditions are satisfied. In this case, the amount accumulated in excess of 15% shall be deemed to have been applied for charitable or religious purposes in India during the previous year itself.

Section 11(2) further liberalizes and enlarges the exemption given under section 11(1)(a). A combined reading of both the provisions would clearly show that section 11(2), while enlarging the scope of exemption, removes the restriction imposed by section 11(1)(a) but it does not take away any the exemption allowed by section 11(1)(a).

Conditions to be satisfied

Exemption under section 11(2) shall be allowed subject to the following conditions being satisfied:

1. Such person furnishes a statement in Form No. 10 electronically either under digital signature or electronic verification code to the Assessing Officer, stating the purpose for which the income is being accumulated or set apart and the period for which the income is to be accumulated or set apart, which shall in no case exceed five years;

2. The money so accumulated or set apart is invested or deposited in the forms or modes specified in section 11(5);

3. The statement referred to in clause (a) is furnished on or before the due date specified under section 139(1) for furnishing the return of income for the previous year.

Section 11(3) in The Income Tax Act, 1961

Any income referred to in sub-section (2) which—

(a) is applied to purposes other than charitable or religious purposes as aforesaid or ceases to be accumulated or set apart for application thereto,

(b) ceases to remain invested or deposited in any of the forms or modes specified in sub-section (5), or

(c) is not utilised for the purpose for which it is so accumulated or set apart during the period referred to in clause (a) of that sub-section.

(d) is credited or paid to any trust or institution registered under section 12AA [or section 12AB] or to any fund or institution or trust or any university or other educational institution or any hospital or other medical institution referred to in sub-clause (iv) or sub-clause (v) or sub-clause (vi) or sub-clause (via) of clause (23C) of section 10,

Shall be deemed to be the income of such person in the previous year-

If the accumulated income is not applied within 5 years, the same shall be taxed in the 5th year itself under section 11|(3)(c).

Up to Assessment year 2022-23, it was taxed in the 6th year under section 11|(3)(c) of the Act.

For example:

In the instant case, the institution accumulated Rs. 25,00,000/- in the previous year 2022-23 for acquiring and developing a land of construction of a new hospital for a period of 3 years. The assessee was required to utilize this amount by 31.03.2026. the assessee has spent Rs. 19,00,000/- (out of accumulated sum Rs. 25,00,000/-) in the previous year 2025-26. Therefore, the unutilized amount of Rs. 6,00,000/- is deemed to be income of the previous year 2025-26 (Related Assessment Year : 2026-27).

Section 11(3A)

Section 11(3A) provides that where the Income invested/deposited in approved modes cannot be applied for the purposes for which it was accumulated or set apart, due to circumstances beyond the control of the assessee, such assessee can make an application to the assessing officer specifying such other purpose for which he wants to utilize such accumulated income. Such other purposes should be in conformity to the objects of the trust. The Assessing officer in this case, may allow the application of such income to such other purposes.

Relaxation under Section 11(2), due to circumstances beyond its control.

Conditions for availing the relaxation;

1. Request the Assessing officer to allow the application to some other charitable purposes.

2. Satisfaction of the Assessing officer that the non-application was beyond the control of the organization.

3. The unutilized amount will be applied for such other objects which are in conformity with the objects of the trust.

Section-11(4) Profits and gains from a business undertaking held under a trust

Section 11(4) provides that a business undertaking held by a trust will be treated as a property held under a trust in the other words for the purposes of section 11. "property held under trust" includes a business undertaking so held, and where the income determined by the Assessing officer exceeds the income as shown in the books of account of the undertaking, such excess shall be deemed to be applied to purposes other than charitable or religious purposes and thus, it will be liable to be taxed accordingly. In other words, if income shown in accounts of such business undertaking is less than income determined by Assessing Officer, then such excess will not be exempt.

Section 11(5) Of Income Tax Act

Section 11(5) of the IT Act deals with the modes of investment prescribed under Section 11 :

• Immovable property investments (not including machinery and plants).

• Investment in as defined in clause (c) of section 2 of the Government Savings Certificates Act, 1959 (46 of 1959), and any other securities or certificates issued by the Central Government under the Small Savings Schemes of that Government;

• Savings certificates and other securities or certificates issued by the Central Government

• Public sector company’s shares are subject to the conditions specified.

• Deposit with a scheduled bank or a cooperative society engaged in banking (including a cooperative land mortgage bank or a cooperative land development bank).

• Deposits in Post Office Savings Bank Accounts.

• Investments in UTI units.

• Securities issued by financial corporations that take part in long-term industrial financing in India are eligible for availing deductions as per Section 36(1)(viii).

• Deposits or investments in any bonds issued by a public company formed and registered in India with the main object of carrying on the business of providing long-term finance for urban infrastructure in India.

• Debentures issued for or by companies for which the Central Government guarantees the principal and interest amount.

• Shares and mutual fund units of National Skill Development Centre.

• Deposits with Industrial Development Bank of India.

• Other modes of investment as per the Central Government.

Text of section 11(5)

The forms and modes of investing or depositing the money referred to in clause (b) of sub-section (2) shall be the following, namely :-

(i) investment in savings certificates as defined in clause (c) of section 2 of the Government Savings Certificates Act, 1959 (46 of 1959), and any other securities or certificates issued by the Central Government under the Small Savings Schemes of that Government;

(ii) deposit in any account with the Post Office Savings Bank;

(iii) deposit in any account with a scheduled bank or a co-operative society engaged in carrying on the business of banking (including a co-operative land mortgage bank or a co-operative land development bank).

Explanation.- In this clause, "scheduled bank" means the State Bank of India constituted under the State Bank of India Act, 1955 (23 of 1955), a subsidiary bank as defined in the State Bank of India (Subsidiary Banks) Act, 1959 (38 of 1959), a corresponding new bank constituted under section 3 of the Banking Companies (Acquisition and Transfer of Undertakings) Act, 1970 (5 of 1970), or under section 3 of the Banking Companies (Acquisition and Transfer of Undertakings) Act, 1980 (40 of 1980), or any other bank being a bank included in the Second Schedule to the Reserve Bank of India Act, 1934 (2 of 1934);

(iv) investment in units of the Unit Trust of India established under the Unit Trust of India Act, 1963 (52 of 1963);

(v) investment in any security for money created and issued by the Central Government or a State Government;

(vi) investment in debentures issued by, or on behalf of, any company or corporation both the principal whereof and the interest whereon are fully and unconditionally guaranteed by the Central Government or by a State Government;

(vii) investment or deposit in any public sector company:

Provided that where an investment or deposit in any public sector company has been made and such public sector company ceases to be a public sector company,

(A) such investment made in the shares of such company shall be deemed to be an investment made under this clause for a period of three years from the date on which such public sector company ceases to be a public sector company;

(B) such other investment or deposit shall be deemed to be an investment or deposit made under this clause for the period up to the date on which such investment or deposit becomes repayable by such company;

(viii) deposits with or investment in any bonds issued by a financial corporation which is engaged in providing long-term finance for industrial development in India and which is eligible for deduction under clause (viii) of sub-section (1) of section 36;

(ix) deposits with or investment in any bonds issued by a public company formed and registered in India with the main object of carrying on the business of providing long-term finance for construction or purchase of houses in India for residential purposes and which is eligible for deduction under clause (viii) of sub-section (1) of section 36;

(ixa) deposits with or investment in any bonds issued by a public company formed and registered in India with the main object of carrying on the business of providing long-term finance for urban infrastructure in India.

Explanation.- For the purposes of this clause,—

(a) "long-term finance" means any loan or advance where the terms under which moneys are loaned or advanced provide for repayment along with interest thereof during a period of not less than five years;

(b) "public company" shall have the meaning assigned to it in section 375 of the Companies Act, 1956 (1 of 1956);

(c) "urban infrastructure" means a project for providing potable water supply, sanitation and sewerage, drainage, solid waste management, roads, bridges and flyovers or urban transport;

(x) investment in immovable property.

Explanation.- "Immovable property" does not include any machinery or plant (other than machinery or plant installed in a building for the convenient occupation of the building) even though attached to, or permanently fastened to, anything attached to the earth;

(xi) deposits with the Industrial Development Bank of India established under the Industrial Development Bank of India Act, 1964 (18 of 1964);

(xii) any other form or mode of investment or deposit as may be prescribed.

Section 11(6) in The Income Tax Act, 1961

In this section where any income is required to be applied or accumulated or set apart for application, then, for such purposes the income shall be determined without any deduction or allowance by way of depreciation or otherwise in respect of any asset, acquisition of which has been claimed as an application of income under this section in the same or any other previous year.

Key note:

Inserted by the finance (No. 2) Act, 2014 with effect from 01.04.2015.

1. The finance (No. 2) Act, 2014 with effect from 01.04.2015 lays down that depreciation will not be considered as application of income if the assets on which depreciation has been charged has already been considered as a part of application of income, earlier.

2. Depreciation shall be permissible on assets bit created out of income

3. Depreciation cannot be claimed if cost of acquisition is Nil.

4. The depreciation rates provided by the Income-tax laws are not mandatory.

5. Section 32 will have no application to charitable organization.

Section 11(7) in The Income Tax Act, 1961

Where a trust or an institution has been granted registration [under section 12AA or section 12AB] or has obtained registration at any time under section 12A [as it stood before its amendment by the Finance (No. 2) Act, 1996 (33 of 1996)] and the said registration is in force for any previous year, then, nothing contained in section 10 [other than [clause (1), clause (23C) and clause (46)] thereof] shall operate to exclude any income derived from the property held under trust from the total income of the person in receipt thereof for that previous year:

[Provided that such registration shall become inoperative from the date on which the trust or institution is approved under clause (23C) of section 10 or is notified under clause (46) of the said section, as the case may be, or the date on which this proviso has come into force, whichever is later:

Provided further that the trust or institution, whose registration has become inoperative under the first proviso, may apply to get its registration operative [under section 12AA] [or section 12AB] subject to the condition that on doing so, the approval under clause (23C) of section 10 or notification under clause (46) of the said section, as the case may be, to such trust or institution shall cease to have any effect from the date on which the said registration becomes operative and thereafter, it shall not be entitled to exemption under the respective clauses.]

[Explanation. - For the purposes of this section, any sum payable by any trust or institution shall be considered as application of income in the previous year in which such sum is actually paid by it (irrespective of the previous year in which the liability to pay such sum was incurred by the trust or institution according to the method of accounting regularly employed by it

Provided that where during any previous year, any sum has been claimed to have been applied by the trust or institution, such sum shall not be allowed as application in any subsequent previous year.

Section 12 of Income Tax Act

"Income of trusts or institutions from contributions"

Any voluntary contributions received by a trust created wholly for charitable or religious purposes or by an institution established wholly for such purposes (not being contributions made with a specific direction that they shall form part of the corpus of the trust or institution) shall for the purposes of section 11 be deemed to be income derived from property held under trust wholly for charitable or religious purposes and the provisions of that section and section 13 shall apply accordingly.

Accumulation of Income

An organisation can accumulate 15% of its income indefinitely. In other words, up to 15% of income can be transferred to the corpus every year. Income accumulated or set apart in excess of 15% of the income where such accumulation is not allowed under any specific provisions of the Act shall be taxable under Section 115BBI. The exemption is allowed to a trust for the income accumulated in excess of 15% subject to fulfilment of certain conditions. This exemption, however, shall be withdrawn if such conditions are not complied with by the assessee.

As per Section 11(2), if a trust is not able to apply 85 per cent of its income in a particular year, it can accumulate the shortfall to be used for religious or charitable purposes within the next 5 years. This accumulation is allowed if the assessing officer is informed about the purpose of the accumulation and the period for which the income is being accumulated. The information is to be furnished in Form 10 at least two months prior to the due date specified under Section 139(1) for furnishing the return of income for the previous year.

Even if a charitable institution is not able to utilize 85% of its income for charitable or religious purposes in India, it shall be deemed to be applied for such purposes in the situations described below. Such deemed application of income shall be considered when the institution furnishes the details electronically in Form9A at least two months prior to the due date specified under Section 139(1) for furnishing the return of income for the previous year.

(a) Where income has not been received in the previous year;

(b) Where income could not be applied due to other reasons.

Taxation of income accumulated u/s 11(2)

The circumstances in which the exemption for the accumulated amount under section 11(2) shall be withdrawn and the year in which such amount shall be taxable have been mentioned below:

(a) If the amount is applied for purposes other than religious or charitable or ceases to be accumulated or set apart for application to religious or charitable purposes. It shall be deemed to be the income of the previous year in which it is so applied or ceases to be so accumulated or set apart.

(b) If it ceases to remain invested in the statutory form of investment specified under Section 11(5). It shall be deemed to be the income of such person of the previous year in which it ceases to remain so invested or deposited.

(c) If it is not utilized for the purpose for which it is so accumulated within the allowed period of 5 years. It shall be deemed to be the income of such person of the previous year being the last previous year of the period, for which the income is accumulated or set apart but not utilized for the purpose for which it is so accumulated or set apart.

(d) It is credited or paid to any other trust or institution registered under Section 12AA/12AB or any other fund, institution, trust, hospital, university or other educational institution, or hospital or any other medical institution referred under Section 10(23C)(iv), (v), (vi) and (via). It shall be deemed to be the income of such person of the previous year in which it is credited or paid to such trust, or institution.

The amount so accumulated by the trust shall be utilized for the charitable and religious purposes for which it has been created. Until its utilization, the amount shall be invested in the statutory forms as specified in Section 11(5). Any use of the accumulated funds for any other purpose or if it is not utilized at all, the exemption allowed in the year of accumulation shall be withdrawn.

Where it is beyond the control of the assessee trust or institution to spend the income for which it was accumulated, the Assessing Officer may allow the trust to apply the income so accumulated for any other religious or charitable purposes provided such other purposes are in conformity with the objects of the trust. In such cases, the exemption, granted to the assessee, cannot be withdrawn and the provisions of Section 11(2) will continue to apply. Assessee may apply to the assessing officer for further extension.

Some of the instances of default where the tax implication imposed by npo

1. Income applied outside India [ section 11(1)(c)].

2. Where an organization fails to apply income after considering it deemed application by filing Form 9A.(under section 11(1B)

3. Where an organization fails to apply income after accumulating it by filing Form 10.[(section 11(3)]

4. Value of any Medical or Educational Services provided to Interested Persons [Section 12(2)]

5. Violation of conditions specified under section 12A(1)

(a) Non-filing of Income-tax Return

(b) Non-obtaining & furnishing of Audit Report

(c) Non-maintenance of books of account as prescribed under Rule 17AA (w.e.f. Assessment Year 2023-24)

(d)Non-applying for renewal of Registration or for making the provisional Registration into a normal registration.

6. Not applying for Re-registration for confirming the modification of the object Clause.

7. Violation of section 13(1)

(a) Income applied for the private religious purpose [Section 13(1)(a)]

(b) Income applied for particular religious community or caste [Section 13(1)(b)]

(c) Benefit to interested person [Section 13(1)(c)]

(d) Investment of funds in an unspecified manner [Section 13(1)(d)].

8. Incidental business activity in excess of 20% of gross receipt [Section 13(8)]

9.Anonymous donations in excess of the exemption limit [Section 13(7)]

Different Tax Rates for NPO

1. Section 115BBI Applicable in case of taxation of Specified Income mentioned in the explanation of section 15BBI at a rate of 30%.

2. When benefits of Sections 11 and 12 are withdrawn for a specified reason, the income will be subject to tax as per section 13(10), read with section 164(2).

3. As of Normal Assessee: - When the assessee has not applied for the registration or approval under the income tax act.

4. Section 115BBC: Tax will be applicable @ 30% without any set-off or deduction under any other head on the anonymous donation received by trust.

Violation by Assesses

Taxing specified @30% u/s 115BBI

Registration to continue and taxing net income under section 13(10)

Registration to be cancelled

Taxing specified @30% u/s 115BBI

The Finance Act, 2022 inserted a new Section 115BBI, to provide a special rate of tax for the specified incomes of trust, which is applicable from Assessment year 2023-24

(a) Income accumulated or set apart in excess of fifteen per cent of the income

(b) Violations section 11(3) , Amount not spend with in five year after filing form no 10

Violation section 11(1B) Amount not spend with in time after filing form no 9A

(c) Income invested in modes other than 11(5)

(d) Benefits to specified persons section 13(1)(.c.)]

(e) Application outside India without Board approval [section 11(1)(.c.)]

Different situation in which the benefit will cease under section 11(1B) and 11(3)

(a) It is applied for purposes other than religious or charitable

(b) It ceases to remain invested in statutory form of investment specified under section 11(5);

(c) It is not utilized for the purpose for which it is so accumulated within the allowed period of 5 years.

(d) Donation to other fund, institution, trust cover to sec 11 and 10(23C) (iv), (v), (vi) and (via).(e)Income is applied for private religious purposes or for the benefit of a particular religious community or a particular interested person which does not endure for the benefit of public as a whole.

Registration to continue and taxing net income under section 13(10)

(a) If the trust or institution does not maintain books of accounts as prescribed by rule 17AA

(b) Return of income has not been furnished within time

(c) Audit report not submitted within time

(d) Commercial activities are carried out by the trust or institution and proviso to clause (15)of section 2 of the Act is applicable.

The income of the trust or institution is to be computed on a net basis as follows

(a) Revenue expenses are allowed

(b) Expenses should be in India

(c) Expenses should be for the objects of the trust or institution

(d) Expenditure should not be from corpus as of 31st March of the previous year

(e) Expenditure should not be from loans and borrowings

(f ) Depreciation on assets not allowed if the cost of asset claimed as application

(g) Expenditure should not be donations to other persons

(h) Section 40A(3)/(3A)/40(a)(ia) shall apply

(i) No deduction in respect set-off of any loss shall be allowed

The most severe violations, the registration of the NPO is cancelled.

(a) Application beyond objects

(b) Non maintenance of books of incidental business

(c) Application for private religious purpose

(d) Benefits to particular religious community or caste

(e) In genuine activity/violation of conditions for registration

(f) Violation of other laws

(g) Incomplete, false, or incorrect application in registration

(h) The registration is not removed from the old regime to the new regime or cancelled by the Income Tax or after getting the provisional not applied for within the time for regular.

Section 115TD

Section 115TD was introduced by the Finance Act, 2016. It provides for the taxation of accreted income of the trust in certain cases. Accreted value of the assets is required to be taxed which is the fair market value of all the assets as reduced by the liabilities

Conversion into any form which is not eligible for grant of registration under section 12AA.

Merger with an entity which is not having similar objectives and not registered u/s 12AA.

Failure to transfer, upon dissolution, all its assets to any other trust or institution registered under section 12AA or approved u/s 10(23C) within a period of twelve months from the end of the month in which the dissolution takes place.

Not applied for provisional / regular registration within time, to be imposed 115 TD/115TE/115TF (In budget 2023)

Conversion into a form which is not eligible for grant of registration’ – Meaning

The specified registration granted to it has been cancelled

It has adopted or undertaken modification of its objects

(i) Has not applied for fresh registration to obtain specified registration in the said previous year

(ii) Has filed application for fresh registration to obtain specified registration but the said application has been rejected

(iii) It fails to make an application for approval in accordance with clause (i)/(ii)/(iii) of first proviso to section 10(23C) or for registration under section 12A(1)(ac)(i)/(ii)/(iii), within the period specified therein, which expires in the said previous year.

Understanding the Concept of Corpus Fund – Treatment Under Income Tax & FCRA ...

New Income Tax Return Filing Requirements for NGOs – Form ITR-7 Explained Legal Framewo...

Income from Business by NGOs: Section 11(4A) Explained Legal Framework (Sections 11(4) and 11(4A...

PUBLIC INSTITUTIONS EXEMPT FROM TAX [SECTION 10] The Income Tax Act of India, under S...